Here’s a look at the latest developments in the mortgage market this week.

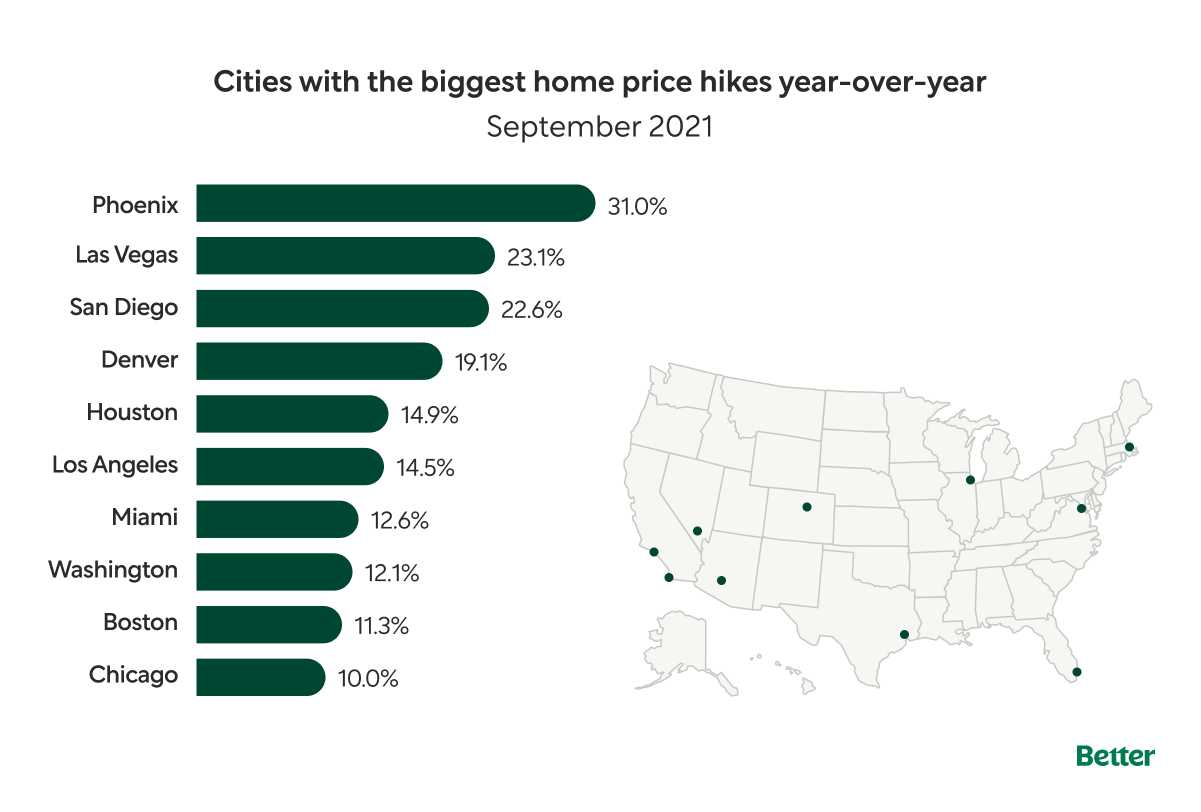

Home price hikes should be slowing down in 2022

Home prices have surged over the last year and a half, but as rates go up and more listings hit the market, that rise is expected to slow down over the course of the next year.

In September, home prices grew by a record 18% year-over-year, with the median price of an existing home shooting up nearly $40,000 in a year. It’s thanks to the squeeze of low supply and high demand, especially in major cities where prices made their biggest leaps.

Source: Corelogic Price Index

Looking ahead, economists expect home prices to rise by only 1.9% between now and September 2022—the lowest increase in a decade. Conditions created by the pandemic will have cooled down: rates will likely be higher, and with much of the country back to work and daily routine, there may be fewer shoppers. Plus, a rush of listings is expected in the next few months to help ease inventory. This may make more room for different price points on the market, which is good news for buyers working with 3%, 5%, or 10% down payments.

For now, the supply gap isn’t even close to being filled, so competition is likely to stay intense. Being ready with your best offer is important, and getting pre-approved is your first step in getting there. See your personalized rates with Better Mortgage for the fullest picture of your options, along with a licensed Home Advisor to chat through the numbers with you. It only takes minutes, and won’t impact your credit score.

Mortgage rates are going up—and expected to rise from here

Mortgage rates are ticking upward, with the 30-year fixed rate average jumping 0.12% to 3.01% this past week. The rise is largely driven by inflation—increased prices of goods and services—along with the latest Fed decision to remove measures that helped keep rates low over the last year and a half.

Better Mortgage analysts expect that rates will keep rising into 2022, likely without surpassing 3.25%. Other industry experts expect the 30-year fixed rate average to peak at just 3.6%. To put those expectations into perspective, the difference between today’s 3.01% rate and the 3.25% maximum can translate to about $3000 on a $300,000 30-year loan.

Rising rates are one more reason why refinancing your home may now may help you save more in the long run. Take a look at your rates to see how much you can take home. If you’re on the fence, crunch the numbers with this refinance calculator to see if it’s the right time for a new loan.

How our idea of “home” is changing with the times

Homes play a big role in our holiday traditions. In the last 5 years, an average of 52 million people travelled home each November to be with loved ones. But as our society, technology, and economy changes, so do the trends in how we buy homes and live in them. From multiple generations of family under one roof, to young professionals splitting homeownership costs through co-housing. There are pros and cons to every living situation, but co-borrowing can help ease some of the challenges that come with owning, maintaining, and financing a home on your own. Read more about what shared homeownership means, and how it’s changing.

Considering a home loan?

Get your custom rates in minutes with Better Mortgage. Their team is here to keep you informed and on track from pre-approval to closing.