What You’ll Learn

The difference between a home’s market value and it’s appraised value

What an appraisal contingency is and why some buyers choose to waive it

How to boost your odds of an accepted offer by 50% or more1

Few people actively want to buy something they know is overpriced. If you’re looking to buy a home, you’d typically want the home appraised to get an objective view of the value of the home. If the appraised value of the home is less than the accepted offer, many buyers are reluctant to pay the full amount of their original offer. That’s why appraisal contingencies are so common in real estate contracts.

When the real estate market gets especially competitive, however, appraisal contingencies can delay closing or prompt a seller to reject an offer outright. That’s why it’s so important to understand what an appraisal contingency is, how a home appraisal affects your mortgage, and when to consider waiving the appraisal contingency altogether.

What is an appraisal contingency and why is it important?

To understand what an appraisal contingency is, we first need to look at home appraisals. A home appraisal is an unbiased opinion of the value of a home. The market value may be different, however, because the market value is determined by how much buyers are willing to pay for the property.

To determine the appraised value of a residence an appraiser compares the home to similar properties that recently sold in the area, much in the same way that the seller’s real estate agent did when they suggested a list price. If the market is particularly competitive, a bidding war can drive up the market value of the home, but an increase in market value doesn’t necessarily translate to appraised value.

Before most home purchases can proceed, conditions need to be met—these conditions are known as contingencies. When homebuyers and sellers agree on the sale price of a home, they typically include contingencies as part of the purchase contract to give each party the option to back out if their conditions aren’t met. Contingencies are often applied to the home inspection, the title of the property, the home sale itself, the financing (known as a mortgage contingency), and the appraisal.

An appraisal contingency protects homebuyers by allowing them to cancel their purchase contract if the home appraisal comes in lower than their offer price. Many buyers are fond of including appraisal contingencies with their offers to make sure they’re not over paying for the property. The appraised value of a home is also important to the buyer's mortgage company because the lender doesn’t want to overpay either.

How appraised value affects your loan

When a lender evaluates what mortgage rate and terms to offer, they also want to make sure they don’t lend more money than the home is worth, this is why the mortgage appraisal process is important to a lender. After your offer on a home is accepted and you lock your rate with a lender, one of the first things they’ll request is a home appraisal because they want to know that they can recoup their money if the home goes into foreclosure.

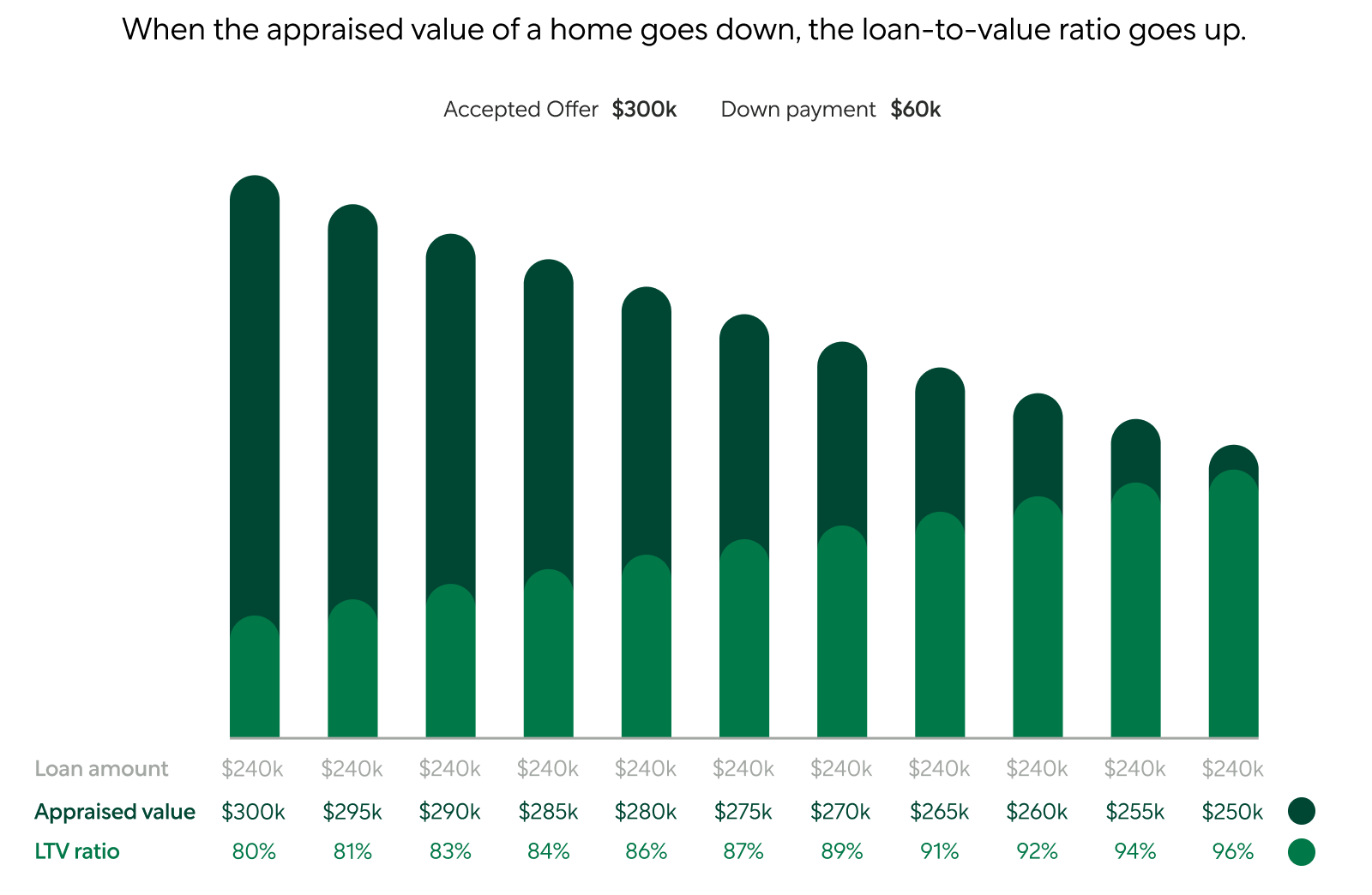

To determine how much risk they’re taking on lenders use the loan to value ratio (LTV) which is calculated by dividing the total home loan amount by the appraised market value of the home. If you make a 20% downpayment on a home, your home equity will be 20% and your LTV will be 80%.

The higher the LTV, the higher the risk for the lender. When your LTV goes up, so do the interest rates you’ll be offered—and if your LTV goes above 80%, you’ll need to pay for private mortgage insurance (PMI) on top of your monthly mortgage payment. (For most mortgages with PMI, your PMI payments will automatically stop once your home equity goes above 22%.)

This graph has been prepared for illustrative purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

If you’re eager to keep more money in your pocket after you pay your mortgage each month, it helps to keep your LTV low. However in a competitive market things can get tricky because the initial loan estimate you receive from your lender is based on your accepted offer on the home and your financial situation.

What if the appraisal comes in low for the buyer?

When a home appraisal value comes back low, homebuyers have a few options:

- Renegotiate the sales price with the seller or ask for concessions.

- Increase your deposit to cover the difference between the appraised value and the accepted offer price.

- Accept new loan terms from your lender.

Although sellers may be willing to renegotiate the sales price in a buyers market or a balanced market, you may find sellers less likely to renegotiate the price of the home if they’re in a competitive market.

If the home appraisal comes in lower than the accepted offer it will impact your LTV. If your LTV goes up, your lender may want to change the terms of your mortgage—most likely by increasing your interest rate. If your LTV goes above 80% you may also need to pay private mortgage insurance.

How often do home appraisals come in low

The difference between the appraised price of a home and the accepted offer price is called an ‘appraisal gap’. In a balanced or buyer’s market, appraisal gaps are not common. In a competitive market, however, they can be something you’ll need to prepare for.

While there are no easy stats on how often appraisals come low, there are indications that suggest appraisal gaps are happening in specific real estate markets. For example, according to Redfin, during the 4 week period ending on March 21, 2021, 39% of homes sold above their list price. Between March and June 2021, 2 San Francisco Bay area homes went for $1M over the asking price. And the share of cash sales among non-first-time buyers has skyrocketed to 33.5% in April 2021.

While homes going over list price is not uncommon, when you see an increase in all-cash offers at the same time, it can indicate that home appraisals in the area are coming in low. Your real estate agent can give you a good idea how common appraisal gaps are in the area where you’re hoping to buy.

Forewarned is forearmed, so if you’re buying in a market where homes are going well over asking, you may want to work with your real estate agent to find homes at a price point that gives you some wriggle room to cover the appraisal gap if push comes to shove. If you’re looking to buy a home for under $822,375 and have a down payment of at least 10%, Better Mortgage and Better Real Estate can give you another way to cover the appraisal gap.

Work with Better to strengthen your offer

Appraisal issues are one of the most common causes of closing delays and from the seller’s point of view, an appraisal contingency gives them less certainty that the sale will go through. This is why sellers who receive multiple offers tend to look favorably toward offers without appraisal contingencies. Better Mortgage and Better Real Estate can help.

By getting your home loan with Better Mortgage and working with an agent from Better Real Estate, you may qualify for the Better Cash Offer1. The Better Cash Offer program allows buyers to waive financing and appraisal contingencies, which gives sellers more confidence. Buyers who are also trying to sell their home won’t be stuck having to pay multiple mortgages or adding in a home sale contingency.

In as little as 3 minutes you can see how much you’ll be pre-approved for with Better Mortgage and get matched with an agent from Better Real Estate. With the Better Cash Offer you will greatly increase your offer strength.