Key highlights

To qualify for a home equity loan or line of credit (HELOC), you'll typically need at least 20 percent equity in your home.

Good credit is essential for HELOC approval, with a credit score in the mid-600s or higher.

Lenders will also consider your debt-to-income (DTI) ratio, with a ratio of 43 percent or lower typically required.

Sufficient income and a reliable payment history are important HELOC loan requirements.

Other financing options, such as personal loans and credit cards, are available if you don't meet the requirements for a HELOC, but generally have higher interest rates.

Use our [HELOC payment calculator](https://better.com/heloc-calculator) to quickly see how much equity you can borrow from your home and what your monthly payments might be.

Introduction

A home equity line of credit (HELOC) can be a valuable financial tool for homeowners looking to tap into their home's equity. Because they are secured by your home, they generally offer lower interest rates than personal loans and credit cards. Whether you're considering home improvements, debt consolidation, or other major expenses, understanding the key requirements for a HELOC is crucial for loan approval.

In this blog, we will walk you through the essential requirements for obtaining a HELOC, from the minimum equity in your home to the necessary documentation for the application process.

In addition, here's a thorough breakdown on everything you need to know about HELOC loans.

Understanding HELOCs

Home equity lines of credit, or HELOCs, are a type of loan that allows homeowners to borrow against the equity in their homes. Unlike a traditional loan, which provides a lump sum of money upfront, a HELOC functions more like a credit card, with a credit limit that homeowners can draw from as needed.

One key advantage of a HELOC is its flexibility. Borrowers can use the funds for a variety of purposes, such as home improvements, debt consolidation, or even education expenses. Additionally, HELOCs often offer lower interest rates compared to other types of loans, making them an attractive financing option for homeowners.

Understanding these key aspects of HELOCs will help borrowers navigate the requirements and make informed decisions about how to utilize their home's equity.

To see today's HELOC rates, click here.

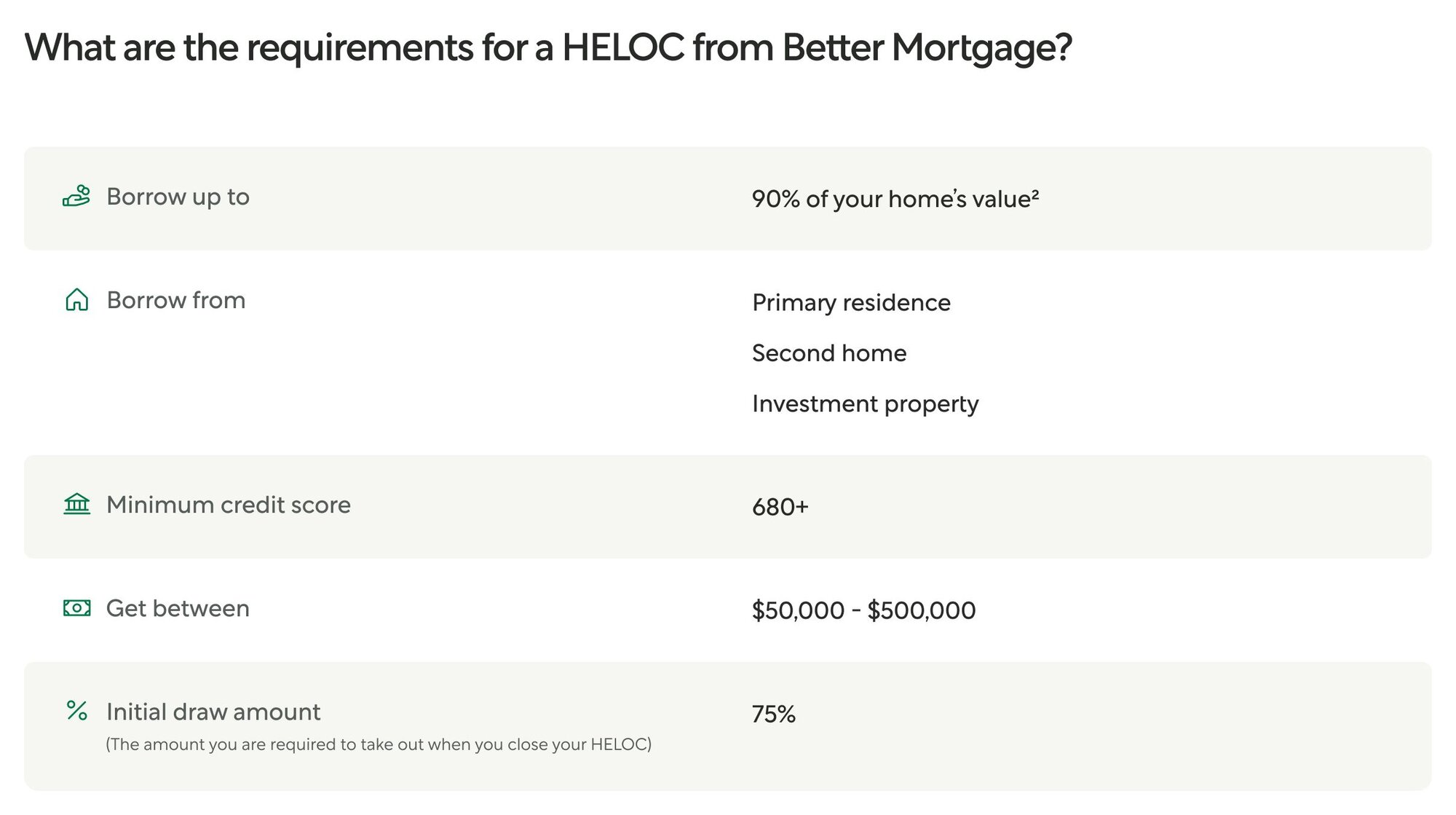

Key HELOC Qualifications

To qualify for a home equity line of credit (HELOC), borrowers must meet several key requirements. These typically include having a sufficient amount of equity in their homes, a good credit score, verifiable income and employment, and a manageable debt-to-income ratio. By understanding and meeting these requirements, borrowers can increase their chances of obtaining approval for a HELOC and accessing the funds they need.

Minimum Equity in Your Home

One of the key requirements for obtaining a home equity line of credit (HELOC) is having a minimum amount of equity in your home. Equity is the difference between the market value of your home and the amount you owe on your mortgage.

Most lenders require borrowers to have at least 15% to 20% equity in their homes to qualify for a HELOC. This equity threshold ensures that borrowers have a significant stake in their homes and reduces the lender's risk.

Credit Score Considerations

Your credit score plays a critical role in the approval process for a home equity line of credit (HELOC). Lenders use your credit score to assess your creditworthiness and determine your eligibility for a HELOC.

A good credit score is typically considered to be at least in the mid-to-high 600s. Lenders want to see a history of responsible credit management, including on-time payments and a low utilization of available credit. A higher credit score not only increases your chances of being approved for a HELOC but also improves the terms and interest rates you may be offered.

In addition to your credit score, lenders will also consider your payment history. A strong track record of making timely payments on your existing debts, including your mortgage, is essential. Lenders want to ensure that you are a reliable borrower who will make consistent payments on your HELOC.

By maintaining a good credit score and a solid payment history, you can improve your chances of obtaining approval for a HELOC and accessing the funds you need.

Verifying your income and employment

When applying for a home equity line of credit (HELOC), lenders will require proof of income and employment to verify your eligibility. Lenders want to ensure that you have a stable source of income to repay the loan.

To verify your income, you may be asked to provide documents such as pay stubs, W-2 forms, or tax returns. These documents demonstrate your monthly income and help lenders assess your ability to make timely payments on the HELOC.

In addition to verifying your income, lenders may also verify your employment. This can be done through contacting your employer directly or requesting additional documentation, such as a letter of employment. Lenders want to ensure that you have a stable job and a reliable source of income.

By providing the necessary documentation to verify your income and employment, you can improve your chances of being approved for a HELOC and accessing the funds you need.

Debt-to-Income Ratio Requirements

Your debt-to-income (DTI) ratio is an important factor in the approval process for a home equity line of credit (HELOC). Lenders use this ratio to assess your ability to manage additional debt.

Your DTI ratio is calculated by dividing your total monthly debt payments by your gross monthly income. Lenders typically want to see a DTI ratio of no higher than 43% to 50%. This means that your total monthly debt payments, including your mortgage, credit cards, and other debts, should not exceed 43% to 50% of your gross monthly income.

To improve your DTI ratio, you can pay down existing debts or increase your income. Lenders want to ensure that you can comfortably manage the additional debt from the HELOC without becoming overburdened.

By meeting the DTI ratio requirements, you can increase your chances of being approved for a HELOC and accessing the funds you need.

Preparing Your Application

Preparing a thorough and complete application is crucial when applying for a home equity line of credit (HELOC). By gathering the necessary documentation and understanding the requirements, you can streamline the application process and increase your chances of approval.

Necessary Documentation for a HELOC

When applying for a home equity line of credit (HELOC), you'll need to provide several key documents to support your application. These documents help lenders verify your financial information and assess your eligibility for a HELOC. Here are the necessary documents you'll likely need:

- Tax returns for the past two years

- W-2 forms or pay stubs to verify your income

- Bank statements to show your financial history and savings

- Proof of your mortgage balance

- Proof of homeowners insurance

By gathering and providing these documents, you can demonstrate your financial stability and support your application for a HELOC.

Tips for a Smooth Application Process

Navigating the application process for a home equity line of credit (HELOC) can be simplified with these helpful tips:

- Maintain a good credit score: A strong credit score increases your chances of approval and may secure better terms and interest rates.

- Gather all necessary documentation: Be prepared by gathering all the required documents, including tax returns, pay stubs, and bank statements, to support your application.

- Research lenders and compare terms: Take the time to research different lenders and compare their terms, interest rates, and fees before committing to a HELOC.

- Follow the application instructions: Carefully read and follow the lender's instructions for submitting your application to ensure a smooth process.

- Be patient: The application process may take time, so be patient and maintain open communication with your lender throughout the process.

By following these tips, you can navigate the application process for a HELOC with confidence and increase your chances of approval.

How to apply for a HELOC

Better Mortgage's HELOC pre-approval application is quick and easy. It takes as little as 3 minutes to complete and makes no impact to your credit score.

How to get a HELOC loan

- Check if you qualify online in minutes with no impact to your credit score.

- You'll see your maximum cash, rates, and expected monthly payments.

- Select a loan and get cash in as fast as 7 days¹

Understanding HELOC Terms

Understanding the key terms associated with a home equity line of credit (HELOC) is essential for borrowers. By familiarizing yourself with terms such as interest rates and repayment terms, you can make informed decisions and effectively utilize your HELOC.

Interest Rates and How They Work

Interest rates are an important aspect of a home equity line of credit (HELOC). Unlike traditional loans with fixed interest rates, HELOCs typically have variable interest rates that can fluctuate over time.HELOC interest rates are often tied to the prime rate, a benchmark interest rate used by banks. As the prime rate changes, so too can the interest rate on your HELOC. This flexibility can result in changes to your monthly payment amount.

Borrowers with a strong credit history and good credit score may be offered a lower interest rate. It's important to compare rates from different lenders and consider the potential for rate increases when evaluating a HELOC.

Understanding how interest rates work with a HELOC can help borrowers make informed decisions and effectively manage their borrowing costs.

Conclusion

Understanding the essential requirements for HELOC approval is crucial when considering accessing your home's equity. Factors such as credit score, income verification, and debt-to-income ratio play a significant role in the approval process. Gathering necessary documentation and maintaining a favorable financial standing can streamline your application process. It's also important to grasp the terms and conditions associated with HELOCs to make informed decisions. By utilizing your HELOC wisely and avoiding potential pitfalls, you can leverage this financial tool effectively. Stay informed about alternative financing options and be prepared to navigate any challenges that may arise during the application process to secure your desired home equity line of credit.

Frequently Asked Questions

Can I get a HELOC with a low credit score?

While it may be more challenging to obtain a home equity line of credit (HELOC) with a low credit score, some lenders specialize in subprime lending and may consider borrowers with lower credit scores. However, approval odds and interest rates may vary.How much equity do I need for a HELOC?

Most lenders require homeowners to have at least 15% to 20% equity in their homes to qualify for a home equity line of credit (HELOC). The equity requirement is based on the loan balance and the appraised value of the home.What are the common reasons for HELOC denial?

Common reasons for home equity line of credit (HELOC) denial may include a high debt-to-income ratio, a poor credit history, and insufficient equity in the home. Lenders assess these factors to determine a borrower's creditworthiness and ability to repay the loan.Is a HELOC or cash out refinance a better option for me?

This depends on several factors — most notably the interest rate on your current mortgage. Learn the difference between home equity loans, home equity lines of credit, and cash-out refinances here. Otherwise, you can use our free HELOC vs cash out refi calculator you can quickly see your estimated payment, rate, and potential savings between the two products.

¹Assumes borrowers are eligible for the Automated Valuation Model (AVM) to calculate their home value, their loan amount is less than $400,000, all required documents are uploaded to their Better Mortgage online account within 24 hours of application, closing is scheduled for the earliest available date and time, and a notary is readily available. Funding timelines may vary and may be longer if an appraisal is required to calculate a borrower’s home value.