What You’ll Learn

How mortgage discount points reduce your monthly mortgage payments

The cost of a discount point and how it varies from mortgage to mortgage

When it’s better to pay for points instead of increasing your down payment

Conventional wisdom suggests that the lower your interest rate, the less you’ll pay for your mortgage. But what if you pay upfront for that low interest rate? Getting the lowest possible interest rate on your mortgage sounds like the holy grail, but paying for mortgage discount points to secure that low rate may not be the best use of your cash in the long run. In some cases you could be better off keeping the original interest rate and putting your spare cash toward your down payment. Knowing how long you plan to keep the mortgage will help you make the right choice for you.

How discount points on a mortgage are computed as a percentage of your loan

Mortgage discount points (also known as ‘mortgage points’ or ‘discount points’) get their name from the term ‘percentage point’. Points are commonly purchased by borrowers to lower their ongoing monthly mortgage payments.

1 mortgage point costs 1% of the total loan amount, in other words, 1 percentage point of the loan.

1 ‘point’ can reduce your interest rate by up to 0.25%, but the actual amount a point will lower your interest rate varies on a daily basis.

As the cost of a point is based on a percentage point of your mortgage, the larger the mortgage, the more it costs to buy a point. For example:

On a $200,000 loan, 1 mortgage point costs $2,000.

On a $600,000 loan, 1 mortgage point costs $6,000.

How mortgage discount points help you save money

Buying mortgage discount points increases your upfront costs in exchange for a discounted interest rate for the full term of your loan. (Most lenders are happy to do this because they know most borrowers don’t keep their mortgage for the full loan term.) When your savings from points cover the cost of the points, you break even, and from that date you’ll start saving money on interest payments. So to make mortgage points worth it, you need to keep your mortgage long enough to break even.

“I have a 20% down payment, should I increase my down payment or pay for points?”

If you have money set aside to cover your closing costs, plus some cash to spare—good for you! Paying for points can save you money long term, but it all depends on how long you plan to keep the mortgage. If you need this question answered now, the Better Mortgage fixed-rate loan comparison calculator can crunch the numbers for you.

Every homebuyer’s financial situation is unique, so let’s look at an example scenario:

Home price: $400,000

Initial down payment: 20% ($80,000)

Mortgage type: 30-year fixed rate

Spare cash: $6,400 (enough to buy 2 points)

On this day, 1 point will reduce their interest rate by 0.25%.

| Interest rate | Monthly payment | Lifetime mortgage cost | |

|---|---|---|---|

| Down payment boosted by $6,400 (to 86,400) Their new down payment is now 21.6% | 3.5% | $1,408 | $506,953 |

| Points bought at a cost of $6,400 for 2 points | 3% | $1,349 | $492,088 |

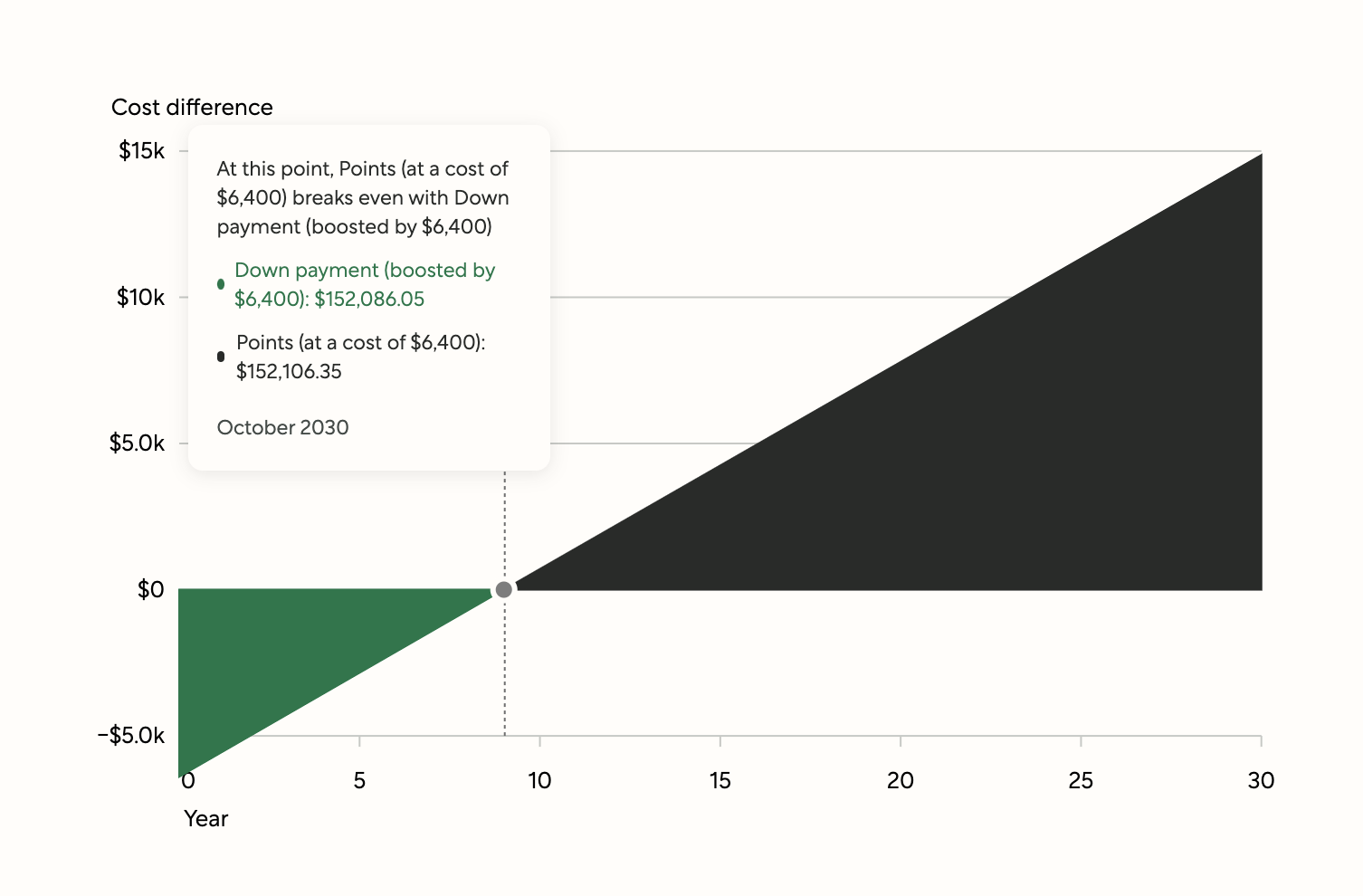

As you can see, putting their spare $6,400 toward points will save this homebuyer money over the lifetime of their loan. However, most homebuyers either sell or refinance their home within the first 10 years of the mortgage, so it’s important to know when the break even point is.

Taking into account the upfront costs and interest, both options cost the same at the 9 year mark.

After 9 years, paying for points (at a cost of $6,400) will be less expensive than boosting their down payment by $6,400. If they plan to sell or refinance before the 9 year mark, the homebuyer should put their spare cash toward their down payment.

“I have a 10% down payment, should I increase my down payment or pay for points?”

If you have a conventional mortgage and a down payment less than 20%, you’ll typically need to pay private mortgage insurance (PMI). The answer to this question is less straightforward when you have PMI because increasing your down payment by 5% of the home’s price can affect the monthly cost of your PMI. In addition, PMI costs are based on your personal financial profile—so it’s always best to speak to a home advisor to get an answer tailored to you.

Let’s see how our example homebuyer’s situation changes if they can only afford a 10% down payment:

Home price: $400,000

Initial down payment: 10% ($40,000)

Mortgage type: 30-year fixed rate

Monthly PMI: $150

Spare cash: $6,400 (for convenience, the cost to buy 2 points is the same as the previous example)

Again, let’s assume 1 point will reduce their interest rate by 0.25%.

| Interest rate | Monthly payment | Lifetime mortgage cost | |

|---|---|---|---|

| Down payment boosted by $6,400 (to 46,400) Their new down payment is now 11.6% | 3.5% | $1,738 $1,588 + 150 PMI for the first 5 years and 2 months / $1,588 for the remaining 24 years and 10 months | $571,616 ($575,616 for the loan + $9,420 in PMI) |

| Points bought at a cost of $6,400 for 2 points | 3% | $1668 $1,518 + 150 PMI for the first 6 years and 2 months / $1518 for the remaining 23 years and 10 months | $564,617 ($553,599 for the loan + $11,018 in PMI) |

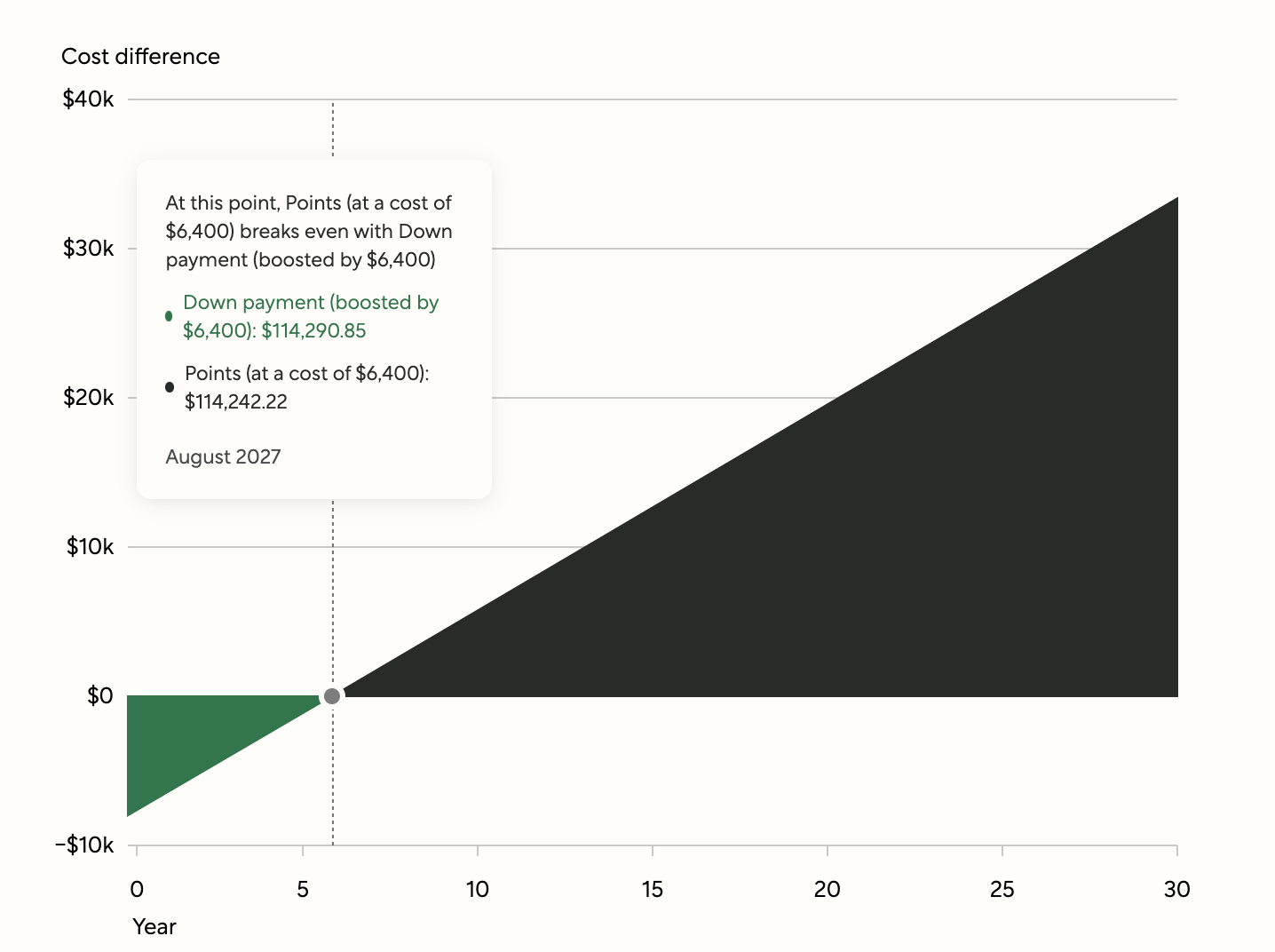

If the borrower put their spare $6,400 toward their down payment, their PMI payments would stop 9 months earlier and they would save $1,598 in PMI costs.

However, if they kept their mortgage for the full 30-year term, they would save more money overall by using their $6,400 to pay for points—this is including the extra 9 months they would have to pay for PMI.

Again, the most important consideration for this homeowner is how long they plan to keep their mortgage.

Taking into account the upfront costs and interest, both options cost the same at the 9 year 6 month mark.

After 9 years and 6 months, paying for points (at a cost of $6,400) will be less expensive than boosting their down payment by $6,400. If they plan to sell or refinance before the 9 year 6 month mark, the homebuyer should put their spare cash toward their down payment.

If you have the money, buying mortgage points could work for you when:

You plan to keep your mortgage for the long term (say, longer than 10 years)

You want a lower monthly mortgage payment to make the payments easier to budget for

Your credit score is preventing you from qualifying for a lower rate

You hope to claim points as an upfront tax deduction

When you apply for a mortgage, the interest rates you’re offered are based on your personal financial situation. Borrowers with higher credit scores, a larger down payment, and less debt are more likely to be offered lower interest rates.

If you plan on keeping your mortgage for a while and you have the cash to spare, buying mortgage discount points could be a great option for you. The first step is to understand what rates you qualify for. A Better Mortgage pre-approval takes as little as 3 minutes and it will show you the budget you have to work with and how your rates and monthly payments change based on how many points you choose to buy. A Better Mortgage Home Advisor will then be able to explain if buying points can help you save in the long run.