Before you lock in your rate and apply for a mortgage, it’s important to understand the options you have available to you, and which ones are right for your situation. There are three key choices you’ll need to make.

- Do you want a fixed or adjustable-rate mortgage?

- Will you pay points or take credits?

- How much will you put towards your down payment?

FIXED AND ADJUSTABLE-RATE MORTGAGES

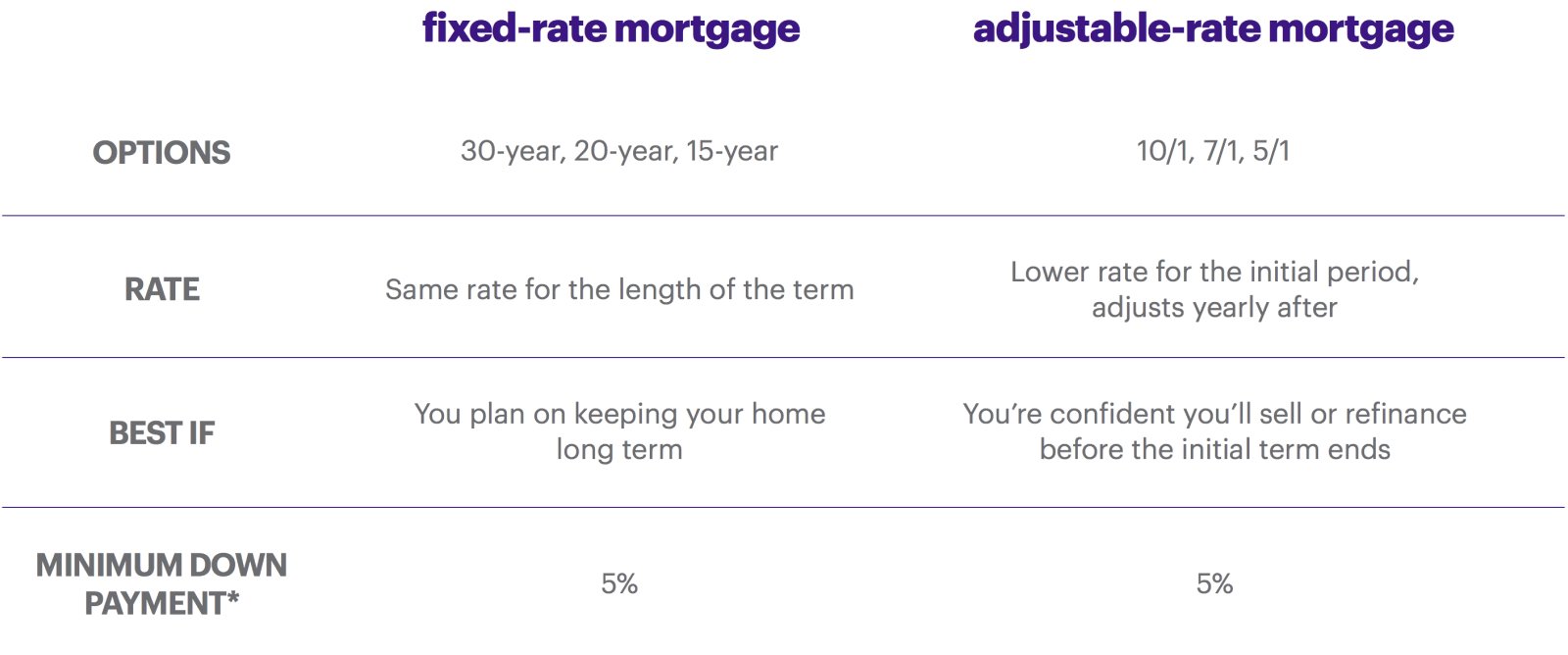

With a fixed-rate mortgage, you’ll have the same interest rate for the life of your loan. No surprises. (Better Mortgage offers 30, 20, and 15-year fixed-rate loans).

With an adjustable-rate mortgage (ARM), you’ll have a lower rate for an initial fixed period (Better Mortgage offers 10/6, 7/6, and 5/6 ARMs). After that initial period is over, rates will adjust (and typically increase) each year, based on market rate factors. Note that there is a predetermined cap that establishes the maximum amount rates can increase each year — so you’ll know the “worst case” scenario going in. (The typical cap is 2% for the initial adjustment period, 2% for subsequent periods, and a 5% lifetime adjustment cap over the initial fixed rate).

*For qualified applicants. In certain cases, Better Mortgage may be able to offer a 3% down payment. Schedule a call with one of our Mortgage Experts to learn more.

If you’re planning on staying in your home long term, a fixed-rate loan is likely the way to go since you can lock in the same rate for the entire length of the mortgage. However, if you’re confident that you’ll be selling within 5-10 years, an ARM could save you thousands. We have some resources explaining how ARMs work and whether they may be a good option for your situation.

POINTS AND CREDITS

- “Taking credits” means accepting a higher interest rate (and therefore higher monthly payments) in exchange for cash to offset your closing costs. If you take enough credits to offset all closing costs, this results in a “no-cost mortgage.”

- The flip side of taking credits is “paying points,” in which you pay some of your mortgage balance upfront in exchange for a lower interest rate (and therefore lower monthly payments).

Whether taking credits or paying points (or neither) is the best option largely depends on how long you plan on keeping your mortgage before refinancing or selling. You can learn more about points and credits and run your own calculations with our interactive tool.

DOWN PAYMENT SIZE

You may have heard that 20% is the magic number for a down payment. It’s true that the greater your down payment, the less you’ll need to borrow, which in turn can mean lower monthly payments and more favorable rates. Putting down 20% or more also means you won’t need to pay private mortgage insurance (PMI) which lenders typically require if your down payment is less than 20%. That said, if 20% down seems unreachable, keep in mind that for people with great credit and a steady income, a 5% down loan can be a financially sound option.

Bear in mind that in addition to your down payment, there will be other third-party fees associated with closing, including your appraisal, title, and flood certification. Some lenders also charge origination or servicing fees (Better Mortgage does not). You’ll also want to make sure you have funds for moving, and possibly renovations and repairs.

If you’re still not sure how to determine which options are best for you, we’re here to help. In as little as 3 minutes, Better Mortgage can show you how much you’re likely to be approved for and match you with a loan consultant to talk through your options.