What you’ll learn ✅

How to calculate your home equity using your home’s value and mortgage payoff amount

How your loan-to-value ratio (LTV) affects your usable equity

Which ways homeowners can turn equity into cash

Tapping into home equity lets you take advantage of one of your greatest assets: your property. Depending on your total share, using equity can be a great way to fund home renovations and college tuitions, but finding that number isn’t typically as easy as using a simple calculator. You need to discover your house’s market value and the remaining balance on your mortgage to know how much equity you have in your home.

This guide explains how to calculate equity in your home, why it’s important, and which ways you can put it to practical use.

What’s the equity in my home?

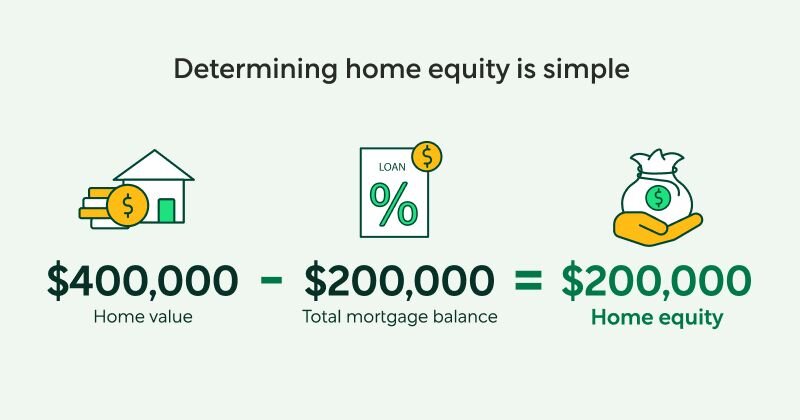

Home equity is the share of your house’s value that you own outright. It’s the difference between your home’s current market value and what you still owe on your mortgage.

For example, if your home is worth $400,000 and your remaining mortgage balance is $240,000, your equity would be $160,000.

As your mortgage balance drops and property values shift with the housing market, that equity often increases. Many homeowners see it grow into one of their largest financial assets — sometimes bigger than savings accounts or investment portfolios.

Your estimated equity gives a starting point for understanding that value. It can guide decisions around renovations, major expenses, and debt consolidation.

How does home equity work?

Equity usually grows in two ways. First, every mortgage payment reduces your loan balance, so more of your home becomes yours. Second, your value can rise with the market or through home improvements you make.

In some markets, prices climb quickly so you can tap into your home value faster than expected. In others, values can dip. Through these changes, the amount of equity on your house can rise or fall based on your remaining loan balance and local home prices.

What’s LTV ratio, and how does it relate to equity?

Your loan-to-value (LTV) ratio compares how much you owe on your mortgage to your home’s current value. Lenders use this number to assess how likely you are to default on your loan. Here’s how to calculate it:

LTV = Mortgage balance / Home value

If you owe $240,000 on a home worth $400,000, your LTV is 60%.

Many lenders prefer total debt on the home to stay below 80% of its value. This shows the owner has more equity, reducing the likelihood that they owe more than the property is worth. Most mortgage providers use this 80% threshold to determine how much equity a borrower can access through loans or lines of credit.

How do I calculate my home equity step by step?

Figuring out equity in your home comes down to a simple calculation using your property’s value and your mortgage payoff amount. Here’s the standard home equity formula, plus a few steps to help you find your number.

Estimate your home’s value

Start with an estimate of what your home could sell for today. Many homeowners use online home value tools for a quick snapshot. These pull recent sales and market trends to give a general range.

You can also ask a real estate agent for a comparative market analysis or order a professional appraisal if you need a precise number.

For simple, early planning, online estimates are fine. However, homeowners typically rely on appraisals when making big decisions like refinancing or accessing a home equity line of credit (HELOC).

Subtract your mortgage balance

Next, find out how much you still have to pay off your mortgage. Keep in mind that this number may be higher than you’d think, as it often includes any interest owed through your entire loan term.

You can usually find your remaining balance in your loan servicer’s online account and in your monthly mortgage statements.

Find your home equity total

Now subtract your mortgage balance from your home’s value.

Home value – Mortgage balance = Home equity

For instance, if your home is worth $375,000 and your mortgage balance is $215,000, your equity would be $160,000.

Understand your usable equity

Even if you have significant equity, lenders typically limit how much you can borrow. This is based on your LTV. Using our above example, say you owe $215,000 on a home worth $375,000. This would make your LTV ratio roughly 57%, putting you in a strong position.

Keep in mind that tapping into home equity is much like securing a primary loan, so lenders will still look into your income and debt-to-income ratio, basing their decision on your equity amount and financial profile.

How can I use my home equity?

Once you figure out how much you have, here are a few ways to get equity out of your home.

Home equity loan

A home equity loan gives you a lump sum of money up front. You repay this amount in fixed monthly payments over a set term much like a traditional mortgage. Many homeowners use these loans for large one-time expenses like renovations and medical bills.

HELOC

A HELOC works like a revolving credit line. Unlike home equity loans, you’re approved for a specific borrowing limit and can draw from it as needed rather than taking all the money at once.

For a period of time, you can withdraw money and only pay the interest on what you borrowed. After this, you can no longer access funds, and payments typically increase because they cover both interest and the initial amount you borrowed.

If you’re looking for a simple way to secure and manage a HELOC, reach out to Better. Access favorable rates, enjoy transparent terms, and handle payments your way.

...in as little as 3 minutes – no credit impact

Cash-out refinance

With a cash-out refinance, you replace your current mortgage with a larger loan and receive the difference in cash.

This approach has pros and cons. For example, it’s a useful tactic if current cash-out refinance rates are competitive and you want to reset your loan terms. However, if your existing rate is lower than today’s benchmarks, refinancing could increase your monthly payment.

Is using home equity right for you?

Using home equity can lower borrowing costs, but it also ties debt to your property. It’s a good idea to weigh the pros and cons to see if this decision makes sense for your situation. Here’s a simple breakdown of the most common benefits and drawbacks:

| Advantages | Disadvantages |

|---|---|

| Lower interest rates than many types of loans | Risk of losing the property if you default on the loan |

| Access to larger amounts of cash | Closing costs may apply |

| Flexible use of funds | Housing market changes can affect equity |

Make the most of your home equity with Better

Home equity can become a powerful financial resource when you understand the numbers behind it. Whether you’re considering a home equity loan, HELOC, or cash-out refinance, Better can help you move ahead.

Better helps you compare your options and pick what works for your goals and budget. Use our fully digital platform to tap into funds and get the most out of your equity. Better’s HELOCs are fast, too — access up to 90% of your home’s value in as little as seven days.

Enjoy a smoother, clearer process with Better.

...in as little as 3 minutes – no credit impact

FAQ

How much equity do you need to sell a home without bringing cash to closing?

To avoid paying out of pocket, you generally need enough equity to cover your remaining mortgage balance plus selling costs like agent commissions and closing fees. Many sellers aim for at least 10% to 15% equity, though this varies by market.

What happens to your home equity when you sell your house?

When you sell, the proceeds first pay off your mortgage balance and any liens. What remains after closing costs is your equity in cash. You may owe capital gains taxes depending on the final price, but you might be able to defer these fees by putting the equity toward another home.