While most homebuyers and homeowners know that their credit score impacts their chances of receiving a loan, many don’t know how their credit score shapes the loan itself. Many lenders have a credit score minimum threshold you’ll need to cross before your application will be accepted (ours is 620), but borrowers between 620 and a perfect score of 850 may see very different rates and terms due to their score and history.

Credit scores are a guideline to help lenders understand how likely a borrower is to fulfill their obligation. The higher the score, the more likely the debt will be repaid. To access your credit score, lenders will need to make an inquiry, sometimes called a “pull,” with one of the three major credit bureaus—Equifax, TransUnion, and Experian, and that inquiry can also impact your credit score. Lenders then evaluate your credit score , along with additional financial information like your debt-to-income ratio, to create your personalized mortgage rate. Borrowers with high scores will see more favorable rates because they’re more likely to repay based on their history. Borrowers with fair to good credit scores may only qualify for higher mortgage rates, but they can bring up those scores by paying down debt, lowering credit card utilization, and avoiding large purchases.

We’ll walk you through all the details so you know what lenders are thinking when they see your score, how to present lenders with the best credit score possible, and feel confident about getting a quick pre-approval (ours takes as little as 3 minutes and doesn’t require a hard credit check).

What is a credit score, and why does a higher score mean more favorable rates?

If you took your entire relationship with debt and boiled it down to a number between 300 and 850, you’d have your credit score. Equifax, TransUnion, and Experian are the three major credit bureaus, but they all use similar criteria to create a credit score. Your FICO score, created by Equifax, is most lenders’ preferred credit score, but all of these scores may be considered when evaluating creditworthiness. When generating your score, credit bureaus weigh payment history, debt volume, the age of your credit, credit diversity (installment based debt like a car loan and revolving debt like credit cards), and credit inquiries. So if you’re monitoring your credit, paying on time, and using less than 30% of your total credit, you should be well on your way to a high score.

Lenders then use that score as a guide to offer interest rates and terms for each borrower. If you think of a loan as a bet, the credit score is the odds of the lender being paid back in full. Rather than denying a mortgage application, lenders adjust the rates and terms to make sure their bet is safe. If a borrower has a high credit score, they can offer more favorable rates and terms because it’s a relatively safe investment. If a borrower has a fair to good credit score, lenders may raise the rates they offer by fractions of a percentage as a way to hedge against a possible default.

Basically, your credit score helps lenders evaluate your ability to pay back your loans, based on your borrowing history. The higher your credit score, the better rates you’ll be able to get, which can lead to significant savings over the life of your mortgage. Your credit score also affects your pricing for mortgage insurance, which is required if you make a down payment less than 20%.

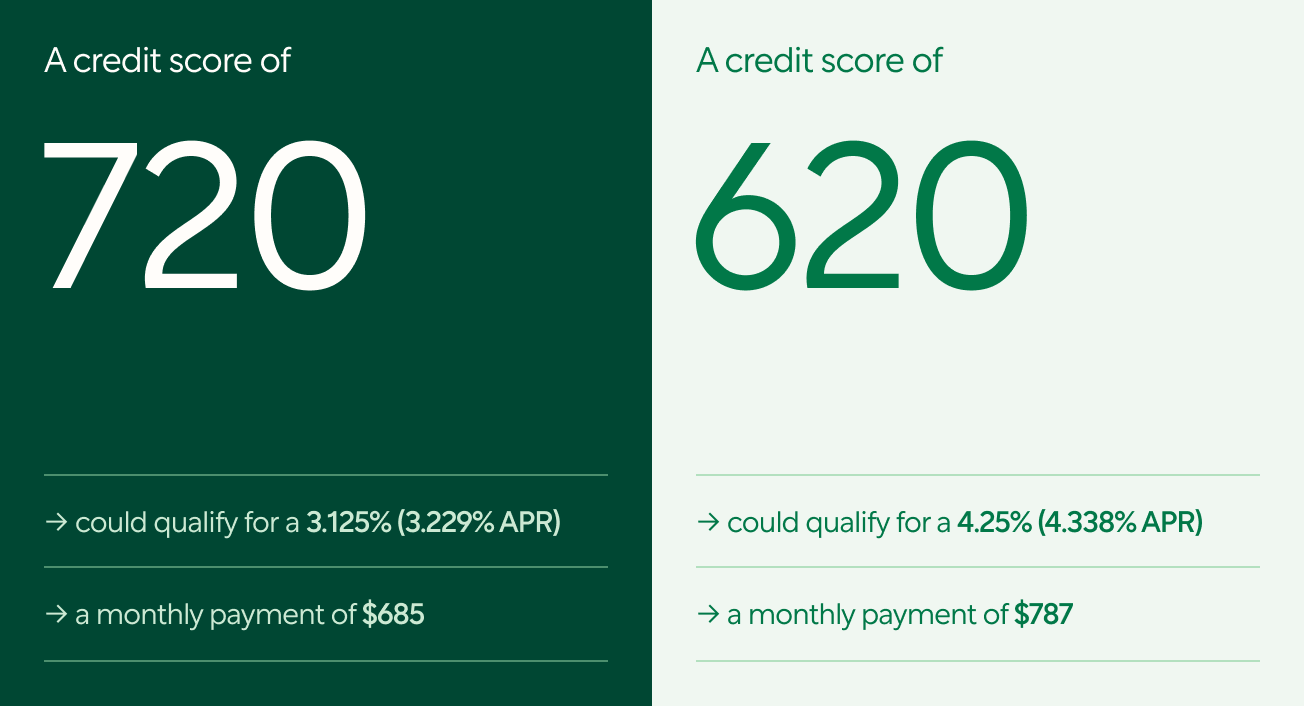

For example: Take a homebuyer with a 20% down payment applying for a 30-year-fixed loan to purchase a $200,000 home in New Jersey.

This scenario is for illustrative purposes only. Calculations are based on a $200,000 single-family primary residence home in Hudson County, NJ using Better Mortgage’s rate tool.

The difference in credit score alone could cost $36,720 over the life of the loan.

Soft credit checks, hard credit checks, and your mortgage

Soft credit checks are checks on your credit that have zero impact on your score. These checks can happen fairly often. For example, every time you go online to check your credit score through a site like CreditKarma or your credit card they conduct a soft check. This way you can monitor your score without damaging it.

The Better Mortgage pre-approval (which takes as little as 3 minutes) can show you how much money you can borrow as well as the rates you qualify for with just a soft credit pull. If you’re in the early stages of home research, you can get a rough estimate of what’s available to you without placing any hard checks on your credit.

Benefits of the Better Mortgage pre-approval and soft credit check:

- Doesn’t affect your credit score

- Shows you your score, so you know what we know

- Allows us to run a monthly debt calculation

- Helps us calculate a more precise number for what you can borrow

- Allows us to quickly run different financing options with you over the phone

Does a mortgage application credit check impact your score?

Hard credit checks are a required part of the formal mortgage application process, and they do come with slight penalties to your credit score (usually around 5 points). The good news is that if you are close to buying or refinancing your home, multiple hard credit checks won’t negatively affect your score multiple times if they all occur within a 45 day period. No matter how many mortgage applications you submit, your credit score will only be impacted once.

| Needed for | Impact on score | Score used | |

|---|---|---|---|

| “Soft” credit check | Basic pre-approval | None | Equifax FICO, Transunion Classic 04 |

| “Hard” credit check | Mortgage application | Usually no more than 5 points (multiple inquiries within 45 days will only affect your score once) | Median scores from Transunion, Experian, and Equifax |

How do multiple credit checks work?

The good news is that if you are shopping around with different lenders, credit bureaus will typically only dock your score once within a 45 day period, no matter how many mortgage lenders do a hard credit check. That’s great if you think you’ll close on a mortgage within 45 days, but if you’re early on in your homebuying process, the clock will start ticking earlier than you may want. Luckily, a Better Mortgage pre-approval doesn’t require a hard credit pull.

You can start your home search with your pre-approved amount, then shop multiple lenders for rates when you’re ready to buy. And if you decide to finance your home with Better Mortgage (great choice!), we’ll only perform a hard credit check once, even if you were pre-approved months before.

This is a great “have your cake and eat it too” strategy when it comes to house hunting. A pre-approval means you’ll start your house hunt with useful information like a budget to work with and a pre-approval letter to show sellers you’re serious. And by waiting until you’re ready to buy to compare mortgages with different lenders, you won’t impact your credit score with a hard credit inquiry or prematurely trigger the 45 day ‘mortgage shopping’ window.

How does applying with a co-borrower work?

When applying with a co-borrower, credit checks will be done for each mortgage applicant. If one co-borrower has a lower credit score, lenders typically use the lower score of the borrowers to determine mortgage eligibility and what rates and terms to offer. For that reason, we often recommend that only the borrower with the higher credit score apply to get the best terms possible. If you decide to apply with a single borrower, you’ll still be able to put both names on the home’s title. If you’re unsure on whether or not you’d like to add a co-borrower,we can help you figure that out.

Take a master class in mortgaging with our free guide.

What credit score will get me approved for a mortgage

At Better Mortgage, we currently provide loans to customers with a credit score of 620 or above (given that other factors like debt-to-income ratio are satisfied). If you have a lower credit score and a flexible timeline, you may want to wait and try and raise your credit score before applying, so you can qualify for a better interest rate. On the other hand, if rates are low and you already have a credit score around or above 720, it may be more financially advantageous to take advantage of a low rate environment rather than waiting to raise your score. It never hurts to see how much you’re pre-approved for and check out today’s rates, especially when our quick pre-approval only uses a soft credit pull.

Mortgage eligibility checker

You can use our rate tool to see what financing you’re currently eligible for and how different credit scores could impact your mortgage rates.

Ways you can improve your credit:

- Keep an eye on your credit score. The Federal Trade Commission has information on how you can get one free copy of your credit report from each of the three nationwide credit reporting companies, and how to dispute errors.

- Pay your balances on time. This is the best way to maintain a good credit score over time. And try to pay more than the minimum payment if you can.

- Keep your credit utilization low. If you can, pay down your credit cards and keep the ratio of utilized to unutilized credit under 30%.

- Keep the oldest accounts open. The longer your credit history, the better. And if you close accounts, you may inadvertently raise your overall credit utilization because you’ll have less credit available to you.

- Limit new credit inquiries. Opening new lines of credit (like an auto loan or credit card) will impact your score for 12–18 months.

- Limit new, large purchases and credit accounts. Keep your eyes on the prize— your home. Wait until after you’ve closed to buy that new car, put new appliances on your credit card, or charge a Hawaiian vacation. All lenders are required to check your credit again before they finalize your loan, so wait until after your loan is fully funded and the keys to your new home are in your hands before increasing your credit utilization, applying for new lines of credit, or closing accounts.

What if your credit score goes up before closing?

First of all, that’s great! All the hard work and financial hygiene paid off. If you haven’t spoken to your lender about locking your mortgage rate (a process where you choose your rate and term and the rate is “locked” in place), then there’s time for your lender to offer you new options based on your score. An increase of just one or two points can change your rate, so it would be worth it to discuss your new score with your lender. If you have already locked your rate, don’t worry. A rate-and-term refinance can help lower your rate in the near future.

Does a mortgage help your credit score?

Yes. Having a mortgage on your credit report actually helps your score. Paying on time, diversifying your debt with installment based debt, and extending your credit history all put you on a path towards good credit. So don’t think of a mortgage as something that can put your credit in danger, but an investment in the future of your credit score. Just make sure you keep your mortgage, as well as your other debts, in good standing and you’ll be in great shape.

Get a Better Mortgage Pre-Approval. It doesn’t affect your credit score.

Whether you’re a 700 or an 825, you may be surprised at how easily you could get pre-approved and for how much. Take our 3-minute pre-approval for a spin (it’ll only take about three minutes) and see what’s available to you. This process uses a soft credit check so it won’t affect your score and it’s a great place to start if you’re looking to buy a new home or refinance your current one.