What you’ll learn

— The reasons you might want to clear your mortgage or invest

— The pros and cons of each approach

— How to use a hybrid model to take advantage of both options

After years of paying down your mortgage and carefully saving, you finally have some extra funds. With that money in hand, a new question may arise: Should you pay off your mortgage early or invest it instead? Many homeowners face this decision, and it can have a big impact on their financial future.

This guide walks through the pros and cons of paying down your mortgage versus investing to help you decide.

What factors should I consider before choosing to pay off my mortgage or invest?

If you’re pondering whether you should pay off your mortgage or invest, here’s a look at the key benefits and drawbacks of each option to consider.

Pros and cons of paying off your mortgage early

Deciding whether to pay off your mortgage early comes with trade-offs. Let’s dive into the main pluses and minuses to help you weigh your options.

Pros

— Boosts attractiveness to lenders: The lower your debt-to-income (DTI) ratio, the less risky you appear to lenders, making you more attractive for future loans.

— Frees up your budget: Are monthly mortgage payments squeezing your finances and getting in the way of other goals? Paying off your mortgage early can free up cash and give you the breathing room you need.

— Saves on interest: Paying off your mortgage before the maturity date can save you a substantial amount of interest, especially if your mortgage rate is high. You can then invest those savings, turning an “either/or” into a “both/and” strategy.

— Prepares you for retirement: If you’re getting close to retirement, eliminating your mortgage takes what’s likely your largest recurring bill off your plate.

— Provides peace of mind: Owning your home outright removes monthly mortgage payments and reduces financial stress.

Cons

— Reduces inflation leverage: A fixed-rate mortgage keeps payments constant while wages and prices rise, lowering the real cost over time. Paying off the loan early stops this effect, meaning you repay the balance sooner rather than benefiting from long-term inflation.

— Removes tax deductions: Once your mortgage is gone, you can no longer deduct mortgage interest on your tax return. In turn, this can increase your taxable income.

— Risks prepayment penalties: Some loans charge fees for early payoff, which can offset some of the financial benefits if your remaining balance is high.

...in as little as 3 minutes – no credit impact

Pros and cons of investing your money

Investing can help your money grow, but it also comes with risks. Here’s a look at the main advantages and potential pitfalls.

Pros

— Takes advantage of employer matches: Contributing to employer-matched retirement accounts earns employer contributions, boosting long-term returns without extra effort.

— Offers tax benefits: Certain investments, like real estate and tax-advantaged accounts, reduce your taxable income. This leaves you with more money to invest.

— Supports long-term growth: Reinvesting returns adds to your capital over time and amplifies potential gains in assets that allow returns to grow.

— Leverages low mortgage rates: If your mortgage carries a low interest rate, your monthly payment will be more affordable. Investing extra funds instead of making higher mortgage payments could earn higher returns over time.

— Maintains liquidity: Keeping some funds in easily accessible investments helps cover emergencies or unexpected expenses.

Cons

— Carries risk: Investments can lose value, which means your principal could shrink instead of grow.

— Exposes you to volatility: Market ups and downs can create stress and tempt you to make emotional decisions that reduce long-term returns. Even without changing your strategy, downturns can lower the value of your portfolio.

— Faces tax implications: Taxes on capital gains, dividends, and interest reduce your net profits. In turn, this limits how much your investments actually earn.

Should I pay extra on my mortgage or invest my money instead?

Crunching the numbers gives you a clear basis for deciding whether to pay off your mortgage early or invest. The key factors are your mortgage interest rate and your expected investment returns.

If your projected profits are lower than your rate, paying off the home loan is likely the smarter choice. But if your expected returns exceed the rate, an investment could be more lucrative. When returns and interest rates are close, a hybrid strategy — splitting funds between extra mortgage payments and investments — can help manage risk.

This example is provided for illustration only; results aren’t guaranteed.

Let’s take a closer look at each scenario.

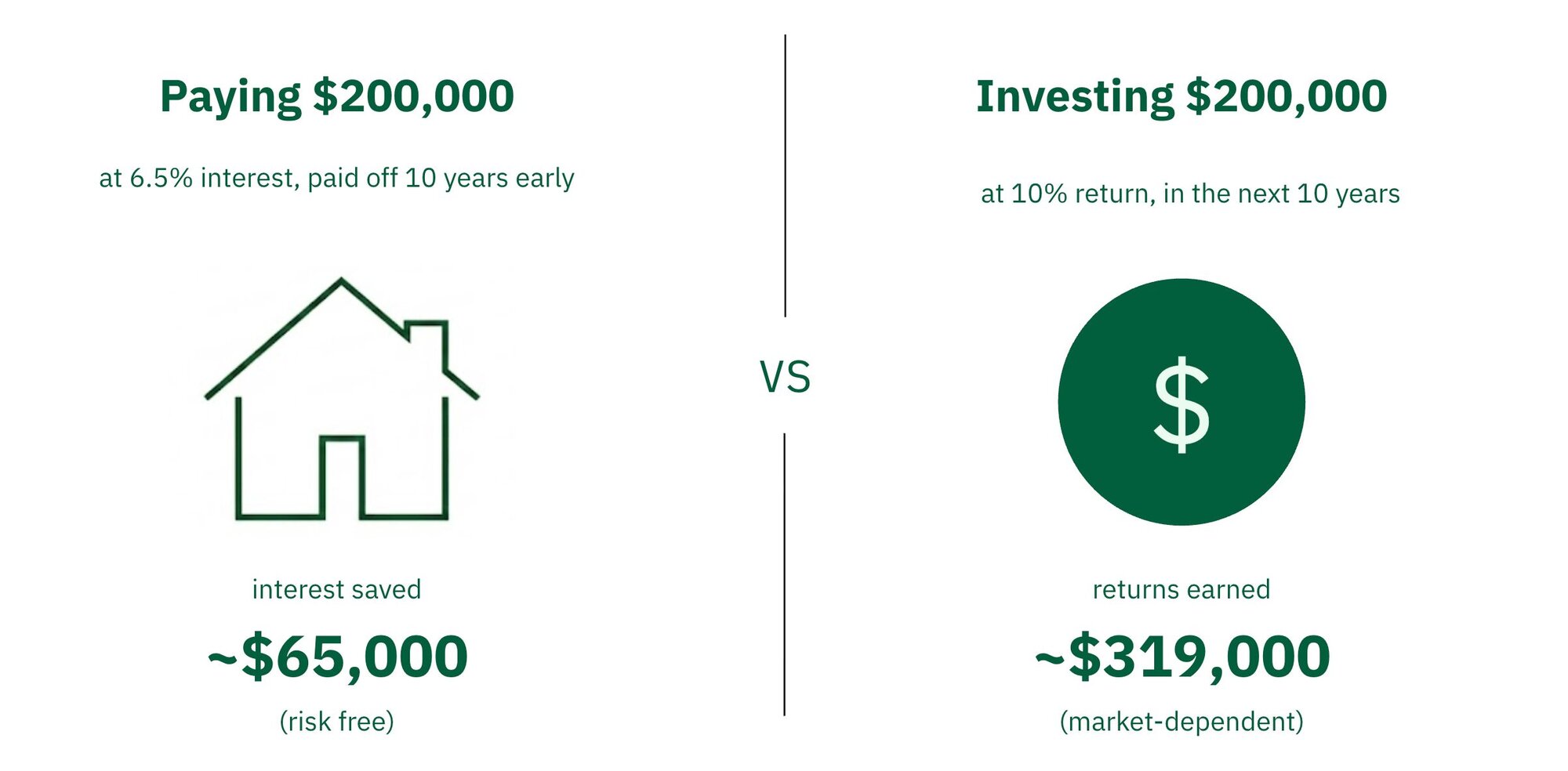

Investing additional funds

Say you have $200,000 left on your mortgage at a 6.5% interest rate and enough extra cash to pay it off without straining your budget. If you instead invest that $200,000 at a long-term average stock market return of 10% per year, it could grow to roughly $520,000 over 10 years. In this case, investing would outperform paying off your mortgage.

Paying off your mortgage early

If your financial advisor predicts below-average returns (say, around 4% per year), paying off the mortgage becomes the smarter choice. In this scenario, eliminating your mortgage would likely save more money than you could reasonably earn through investing.

Taking a hybrid approach

If expected returns are near 6%, close to your interest rate, a balanced strategy may make sense. You could direct some funds toward extra mortgage payments and the rest toward investments, giving you both interest savings and growth potential. Always remember that investing carries risk and no guaranteed returns, while paying off your mortgage can reduce costs with relatively low risk.

How to pay off your mortgage while still investing at the same time

You don’t have to pick just one path. Pairing extra mortgage payments with smart investing gives you both financial stability and growth potential. Here’s how to pay down your mortgage while investing at the same time:

— Accelerate mortgage payments: Make extra payments or switch to a biweekly schedule to reduce your principal faster and shorten your loan term. At the same time, consider investing a portion of extra funds to grow your portfolio, balancing debt reduction with potential investment gains.

— Refinance your mortgage: Lower your interest rate or adjust your term to reduce payments, freeing up cash to invest. Better’s online platform makes this simple. Homebuyers can get pre-approved in as little as three minutes with zero origination, application, or underwriting fees.

...in as little as 3 minutes – no credit impact

Score an affordable mortgage with Better

Weighing the long list of pros and cons to decide whether to invest or pay off your home loan can be tough, but choosing a lender doesn’t have to be. Better is one of the most trusted mortgage lenders in the game. We’re the first fintech company to fund more than $100 billion in loan volume. Applying is free, fast, and has no strings attached — so what are you waiting for?

Get pre-approved today, and see how much you could save.

...in as little as 3 minutes – no credit impact

FAQ

Is it better to pay off a mortgage or invest?

The starting point for deciding whether to go for a mortgage payoff or an investment plan is comparing your mortgage rate to your expected gains. If your mortgage rate is steep, paying down your loan early might make more sense, while stronger projected returns make investing potentially more worthwhile.

Key factors to consider include:

— Assess risk tolerance: Paying off your mortgage reduces debt and interest costs, but it isn’t completely risk-free. If you have low risk tolerance, investing may feel more stressful than it’s worth.

— Evaluate liquidity needs: Stocks and bonds usually provide liquidity, though some may have restrictions or limited market access.

— Consider your time horizon: If you plan to move soon, paying off your mortgage won’t save much on interest.

Should I pay off my mortgage if I have other debts?

It depends on the type of debt. Focus on high-interest debts, like personal loans and credit cards, before putting extra funds toward your mortgage to reduce costs over time.