What You’ll Learn

The advantages and disadvantages of renting versus buying a house

What factors go into a rental and mortgage approval

Why buying a home may be more affordable than you think

Are you thinking about making the switch from renting to buying a house? Maybe you're sick of paying off someone else's mortgage, you want to start building equity, or you simply want a home that feels more like yours. Whatever the reason, there’s a lot to consider before jumping into homeownership. Let’s cover the advantages and disadvantages of renting versus buying a house, so you can figure out what works best for your finances, lifestyle, and future plans.

Pros and cons of renting vs buying a house

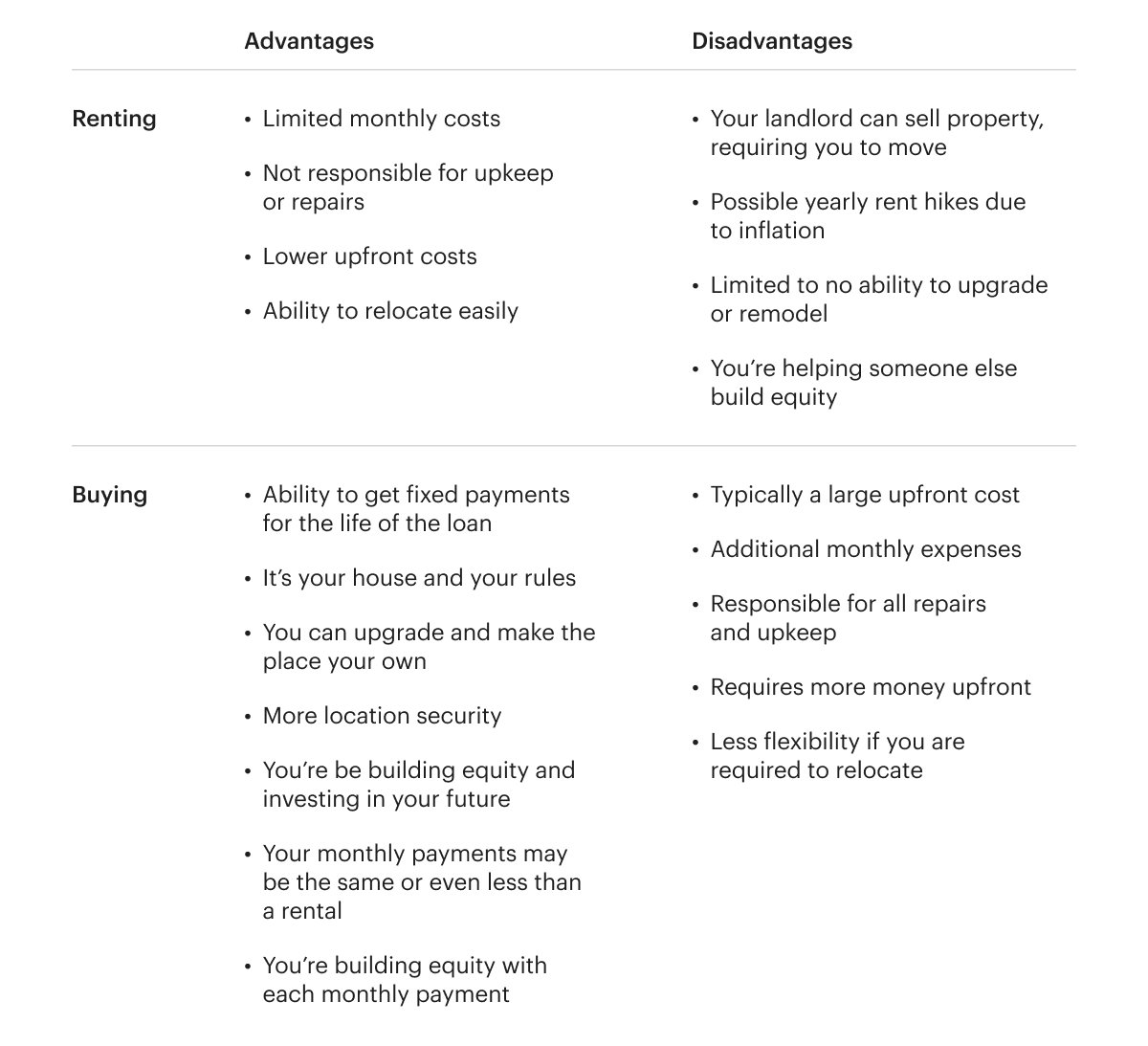

Advantages of renting a house

Fewer costs and responsibilities

When renting a home, you're only responsible for paying your monthly rent and any utilities that aren't included. You're not on the hook for typical homeowner-related costs, such as property taxes, home maintenance, or repairs. If a screen door breaks or the roof springs a leak, you can simply call the landlord to have it fixed—usually with no money out of pocket.

Lower upfront costs

Purchasing a home comes with a whole bunch of upfront costs that you won’t have to pay for a rental. In fact, some rental properties have no upfront costs at all. At most, you may have to pay an application fee and/or a security deposit before you move in. Application fees vary from state to state but are typically less than $50. A security deposit is usually between one and three month's rent, depending on where you're looking to move.

Keep in mind, you should be able to get your security deposit back, as long as you keep the property in good condition. If you’re expected to pay your first and/or last month’s rent in advance, then your money’s not going to waste, either; you’re simply getting ahead of future rent payments.

All in all, the upfront costs associated with moving into a rental property are much less than what it costs most homebuyers for a down payment, closing costs, and property taxes.

Relocation flexibility

Because rental leases are designed for the short term, you’re not tied down if your life circumstances suddenly change. For example, if you want to take a job opportunity in a new city, it’s much easier to break a lease than it is to sell a home.

Disadvantages of renting a house

The landlord calls the shots

Notice periods

Renting doesn’t come without risks. Landlords can decide to sell their home or make it unavailable to rent whenever they choose, leaving you to find new living arrangements. Look closely at your rental agreement or lease to understand the notice period, or how much time in advance your landlord must notify you, should they choose not to renew your lease or plan to vacate tenants.

Rent increases

Landlords often raise rates to keep pace with rental prices and demand in the area or to offset inflation. That means once your original lease is up, you could be forced to accept the higher rate or move again. In 2019, 78% of renters reported a rent increase and more than half said it affected their decisions to move.

Limited ability to customize your space

Renting may leave you with little room for upgrades to your space. Most landlords don’t allow or will require approval for modifications, such as painting walls or even hanging artwork. If you do make changes, it will likely be up to you to put everything back to the way it was by the time your lease is up, or you could forfeit your security deposit.

You’re investing in someone else’s future

When it comes down to it, the biggest drawback of renting is that you’re paying money that goes directly into your landlord's pocket. Even if they have to pay a mortgage on the property, they are still earning home equity as they pay down the loan principal and the property appreciates in value. Meanwhile, you won’t get any benefits beyond being able to stay put for another month.

While it may not seem like a big deal, rent payments add up. According to Apartment Guide’s most recent Annual Rent Report, the average monthly rent for a 2-bedroom apartment in 2019 was just over $1,800. That means after a one-year lease, you would have paid more than $21,600 in rent—for which you’d receive no benefit of equity or ownership.

If that seems like money you’d rather put toward a property of your own, one that generates potential long-term equity and wealth, then read on.

Advantages of owning a house

More location security

As a property owner, you get to decide how long you’d like to live in your home—and when you’d like to sell. This can be especially important if you need longer-term security in a fixed location. For example, if you have or are planning to have kids, you may want to remain in a specific school district for the foreseeable future. Owning a home makes it easy. Renting, on the other hand, doesn’t come with that same level of security; you may have to suddenly find a new home in a new location if your landlord decides to sell.

According to a study by Betterment, it takes an average of 4 years to recoup the upfront cost of buying. So, think about how long you plan to stay in the home.

Payment stability and ownership

If you have a fixed-rate mortgage, you’ll also have peace of mind that your payments won’t go up every year—unlike renting a home where you may see annual rent increases. While your home’s property taxes and insurance may fluctuate, your principal and interest will remain the same for the full term of your home loan. For example, if you have a 30-year fixed-rate mortgage, your payments will remain the same for the full 30 years, regardless of property values, inflation, or rising interest rates.

In some areas, you may even find that your mortgage and homeownership costs are comparable to rent payments, but you get the added benefit of actually owning your home and building equity.

Flexibility to renovate and reap the rewards

When you own a home, you can let your HGTV home goals run wild. You can paint the cabinets, change light fixtures, and even remove walls for some open-concept living. Not only that, but as you make renovations to improve your home, you may also increase its value, depending on the kind of renovation. This can be beneficial if you decide to move or refinance in the future, or simply want the home to increase in market value when compared to other homes in the area.

You’ll be investing in your future

Every time you make a mortgage payment, you are building equity in your home. Equity is the difference between the current market value of the house minus the remaining balance of any outstanding loan.

As your mortgage balance decreases, the amount of equity you have in the home increases. But this isn’t the only way equity can grow.

Appreciation, which is the influence of the market upon value through demand, inflation, or both, can also cause equity to grow. For example, the market value of your home may increase when comparable homes in your neighborhood begin to sell for more than what you originally paid. And because inflation cannot affect the balance of your loan, equity may increase exponentially.

Eventually, you may wish to leverage that equity to buy a second home or fund other financial goals or investments—such as making improvements to your home. (Incidentally, this is another great way to increase home equity.)

Disadvantages of owning a house

Full responsibility and expenses

With added freedom comes added responsibility. As a homeowner, you’ll be the one on the hook for all the costs of owning a home, including the mortgage payment, property taxes, and utilities. You'll also be responsible for the upkeep and maintenance of the property. If something breaks, it's up to you to fix it or to call in someone who can do the job for you—for a cost, of course.

Nomad no more

Once you buy a home, you’re rooted to that house’s location. If you receive an offer for your dream job in another state or decide to move in with a significant other, it can be harder to make that move if you must first sell your home or convert it to a rental property.

Higher upfront costs

When buying a home, you’ll not only need to be able to qualify for a mortgage, but you’ll also need to pay for more out-of-pocket expenses.

In most circumstances, you should account for the following:

- A down payment: Typically 3–20% of the home purchase price

- Closing costs: Typically 2–5% of your loan amount (make sure you don’t end up paying unnecessary lender fees)

- Property taxes and homeowners insurance: You may have to pay for a portion of your real estate taxes and insurance premiums at closing

Renting vs. buying a house: advantages and disadvantages

Approval for rent versus a mortgage

Renting a home

Before being approved for a rental application, a landlord will likely run a credit check to verify you have a history of paying your bills and debts on time. However, this is usually the extent of the financial background check needed to be approved for your home rental agreement.

Buying a home

For most people, buying a home means applying for a mortgage to go with it. And because a mortgage is usually a long-term commitment, your lender will want to ensure that you cannot only afford your monthly payment and housing expenses now, but also for the foreseeable future. To determine your eligibility, lenders will take a detailed look at your finances, including:

Credit score: Most lenders have a minimum credit score requirement for home loans. Generally, the higher your credit score, the lower the interest rate you'll be approved for on your mortgage—which could equate to thousands of dollars saved over your mortgage term. Do your best to raise your credit score as much as possible before you apply for a loan, so you can take advantage of today's historic low rates.

Down Payment: It used to be fairly standard for mortgage lenders to require a strict 20% down payment for any home loan. Thankfully, times have changed and homes have become a lot more affordable than you may think. In fact, some loan programs require down payments of just 3–5% of the home's purchase price. In this case, a $200,000 home would require as little as a $6,000 down payment. Note: While down payment requirements are a lot less stringent than they used to be, you will have to pay for private mortgage insurance (PMI) if you put anything less than 20% down.

Debt-to-income ratio: Lenders use your debt-to-income (DTI) ratio to determine if you can afford to take on more debts in the form of a mortgage. You can find this ratio by adding up your total monthly debts and dividing that amount by your gross monthly income. Typically, lenders will accept DTIs of below 45%.

Loan-to-value ratio: In real estate, your loan-to-value (LTV) ratio is a measure of how much you've borrowed versus how much your home is worth. In general, if you have a loan-to-value ratio greater than 80% (meaning you’re putting less than 20% down), then you may be required to pay private mortgage insurance (PMI) on top of your monthly mortgage payment. This lowers your lender’s financial risk, allowing them to make homeownership an option for people without the cash for a traditional down payment.

How Better Mortgage can help

Deciding between renting versus buying a house is never easy, but today’s low interest rate environment and low down payment options may make homeownership more attainable than you might think. It all starts with getting an understanding of your finances and what you can afford. We can walk you through each step—from planning to closing—with our definitive homebuying checklist. And once you’re ready to start your homebuying journey, Better Mortgage can help. With just a few pieces of information, we can provide you with a quote for how much you’ll likely be approved to borrow. Plus, we never charge unnecessary lender fees, such as loan officer commissions or application, loan origination, and underwriting fees.

See what you can afford or reach out to one of our qualified mortgage professionals to learn more about your options and today’s low rates.