What You’ll Learn

What a mortgage rate lock means for your refinance

How economic conditions can impact mortgage rates

Tips for knowing when to lock your rate

So, you’re officially pre-approved to refinance your mortgage and, after shopping around a bit, you’ve found some interest rates that look favorable. But rates can fluctuate, and the rate you see now might change to something completely different between the time you apply for your refinance and your actual closing date.

In theory, it makes sense to “lock” your interest rate and stabilize the cost of your mortgage until you close. The flip side of this logic is that you risk losing out on savings if rates go down. So, the question is: Should you lock your refinance mortgage rate today? Or is it worth holding out in the hopes that rates drop even further?

The short answer is that it's never a good idea to try to time the market, and if you can achieve your refinancing goals with the initial interest rates in your quote, you should lock today. Here’s a quick breakdown on why you shouldn't gamble when it comes to interest rates.

What’s a rate lock and why do I need one?

A rate lock is when your lender agrees to honor a particular interest rate by “locking” it into your loan for a certain amount of time—typically 30-60 days, or long enough to move your loan through the underwriting process. The idea is to protect you from potential rate spikes that could impact the monthly cost of your refinance. A rate lock makes it possible to close with confidence by ensuring that market changes won’t impact the terms of your loan.

Having said that, you’ll also need to maintain your eligibility for the interest rate throughout the underwriting process. Any significant changes to your financial profile (such as taking on more debt or opening a new line of credit) could have an adverse impact on your credit score or debt-to-income ratio and ultimately prevent you from qualifying for a rate, even if you were initially approved for it. That’s why it’s generally best to hold off on any big purchases until after you refinance your loan.

Should I wait to lock my rate?

You usually have the option to lock your rate as soon as you get the initial approval for your refinance. However, if you’ve been following housing market trends for the last year, you know that rates have hit historic lows on multiple occasions. Because of this, you might feel reluctant to lock in the first rate you get offered—after all, what if a lower rate comes along and you miss out on an even sweeter deal? Rate shopping might sound tempting, but it isn’t recommended.

Market rates are determined by a number of complex variables. Drops and spikes are impossible to anticipate, and even small fluctuations can have a major impact on the amount you pay over the life of your refinance. Instead of trying to game the market, you should lock as soon as you get a rate that can deliver the financial goals of your refinance. Here are some benefits of locking your rate today:

Rates aren’t likely to drop any further anytime soon

Experts agree that rates are unlikely to drop significantly this year. As the economy continues to stabilize, rates are more likely to be on a slow and steady rise throughout 2021. Although rates do go up and down day to day—sometimes even hour to hour—major fluctuations are not the norm. If your strategy is to try and nab a lower rate at the last second, you’re taking a gamble. No one can predict how the market will shift. By waiting, you could just as easily get stuck with a higher rate that could drive up the total cost of your loan over time.

Refinancing is about your personal financial goals

If you’re hoping to refinance this year, you should focus on locking your rate when it makes financial sense for you—i.e., when you stand to save money or when the monthly payment is within your budget. If you can achieve your financial goals with the rates you have available, do it. It doesn’t make sense to hold off for possible greater savings when you could be jeopardizing a guaranteed favorable rate on your refinance. Don’t look at locking your rate as a limiting move—in fact, even after locking you still have some flexibility to finalize loan and application details.

There’s no limit on how many times you can refinance

If the market experiences a significant shift, or if your own financial situation improves, there’s nothing stopping you from taking advantage of it with another refinance. That’s because there’s no limit on the number of times you can refinance. This doesn’t mean you should plan to endlessly refinance—after all, there are costs associated with the process, and it may take time to hit your break-even point. However, you do have options in the event that a major opportunity arises and you want to try and improve the terms of your mortgage.

You might have to spend more if you lock later

If you decide to wait and see if a lower rate comes along, you might miss the deal that’s right in front of you. If market rates increase, you could be faced with the prospect of paying more money upfront to secure the lower interest rate you had initially. You can do this by purchasing “points” to buy down the interest rate on your loan—typically one point costs 1% of your mortgage amount and will reduce your interest rate by 0.25%, so you’ll need to run the numbers on how leveraging points will impact the overall cost of your loan. Alternatively, you might have to bite the bullet on a higher interest rate and pay more in the long run. Even a 0.25% difference can add up to be tens of thousands of dollars over the life of your loan, so it’s safer to lock when you find a rate that works for your financial goals.

Ultimately, it all comes down to your breakeven point

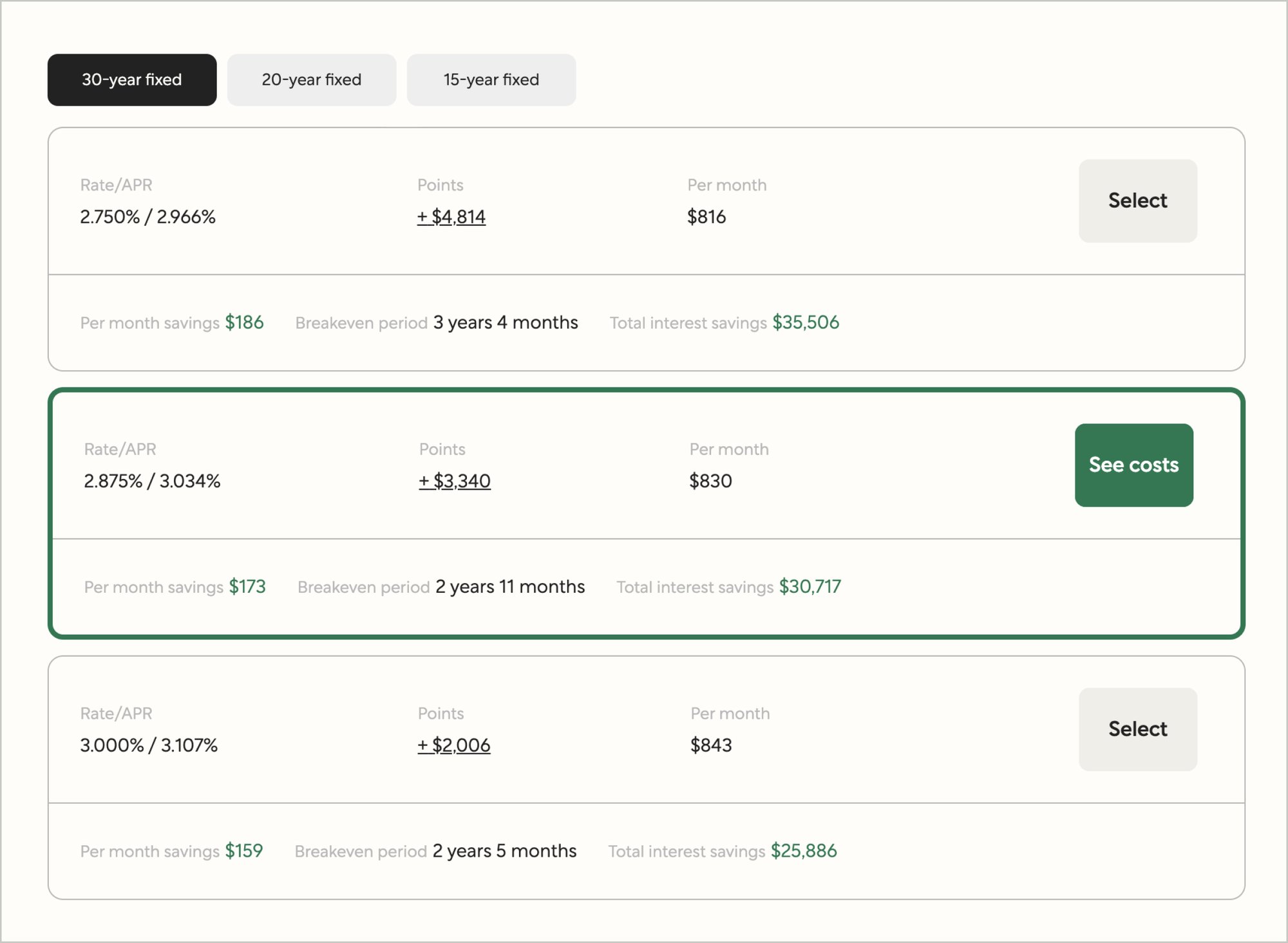

The best way to figure out if you should lock your quoted rate is to calculate your “break even” point, aka when the monthly savings of your new loan will offset the upfront closing costs associated with refinancing. To do that, you need to add up the cost of refinancing (things like title, appraisal, third party fees) and then divide that sum by your monthly savings.

For example, let’s say the cost of refinancing your loan shakes out to $4,000, but you’re locking in an interest rate that lowers your monthly mortgage payment by $150 per month.

$4,000 divided by $150 = 27

In this case, locking the rate is probably a good idea if you’re planning to stay in the home longer than 27 months, or long enough to cover the original cost of the refinance. Better Mortgage provides a clear and transparent look at your refinance savings per month, along with your breakeven point and the total you stand to save in the long run.

This image is for illustrative purposes only

Why you should refinance with Better Mortgage

There are a lot of “what ifs” that come with the refinancing process; don’t let your interest rate be one of them. Rates will fluctuate, but economic conditions that impact rates are typically slower moving, and these swings aren’t generally material enough to justify rate shopping. If the monthly payment fits your budget and makes financial sense for you, you should consider locking your rate today.

When you refinance with Better Mortgage, you’ll be able to see the monthly payments and savings for each rate so you can easily compare and understand exactly what you’re getting. Unlike traditional lenders we don't charge commissions or lender fees, and you can lock your rate at any time. You can also connect with a Loan Consultant to talk through your final rate options so you can feel confident about your decision. Ready to get started? It only takes a few clicks—and a few minutes—to lock your rate with Better Mortgage.

This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.