What you’ll learn

What mortgage points are and how they work

How to calculate mortgage points savings

Steps to determining if mortgage points make sense for you

What are mortgage points?

When buying a home or refinancing your mortgage, you may encounter the option of paying for mortgage points. But what exactly are mortgage points, and how do they affect your loan?

Let’s dive into the details of mortgage points, how they’re calculated, and how they can save you money in the long run.

Understanding points on a mortgage

Mortgage points, also known as discount points, are fees you pay upfront to reduce your mortgage interest rate. In essence, paying for mortgage points allows you to "buy down" your rate, which can lower your monthly payments and potentially save you thousands over the life of your loan.

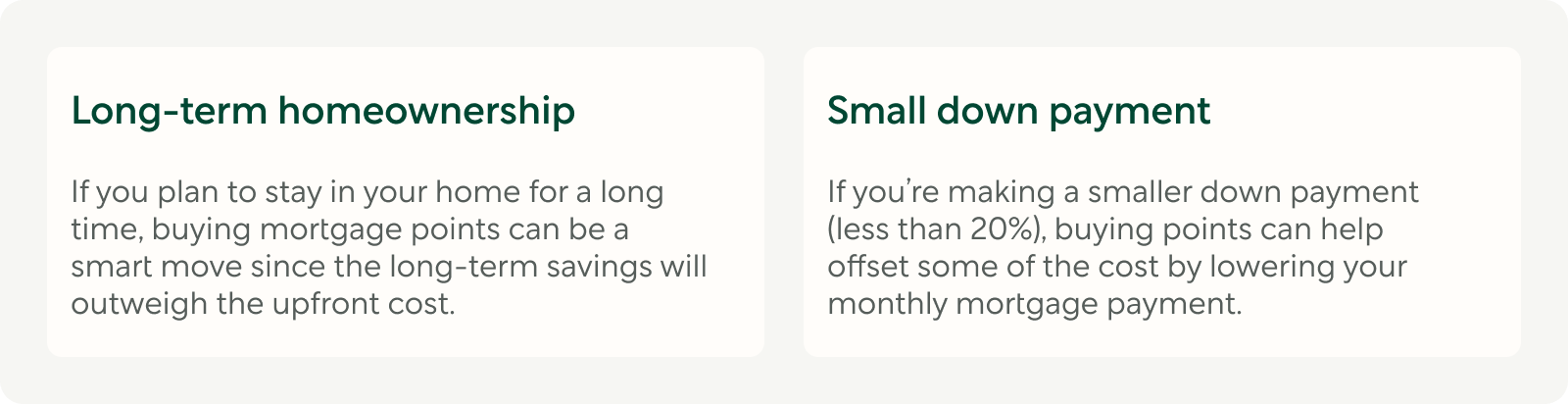

While it might seem counterintuitive to pay more upfront, the decision to buy mortgage points could be a smart financial move if you plan to stay in your home long-term.

Here's everything you need to know about what mortgage points are and how they can impact your mortgage costs.

How are mortgage points calculated?

A mortgage point typically costs 1% of your total mortgage amount. For example, if you're taking out a $200,000 loan, one mortgage point would cost you $2,000. In exchange for paying for the point, your lender will typically lower your interest rate by about 0.25%. This can vary based on the lender and market conditions.

Mortgage points calculation example

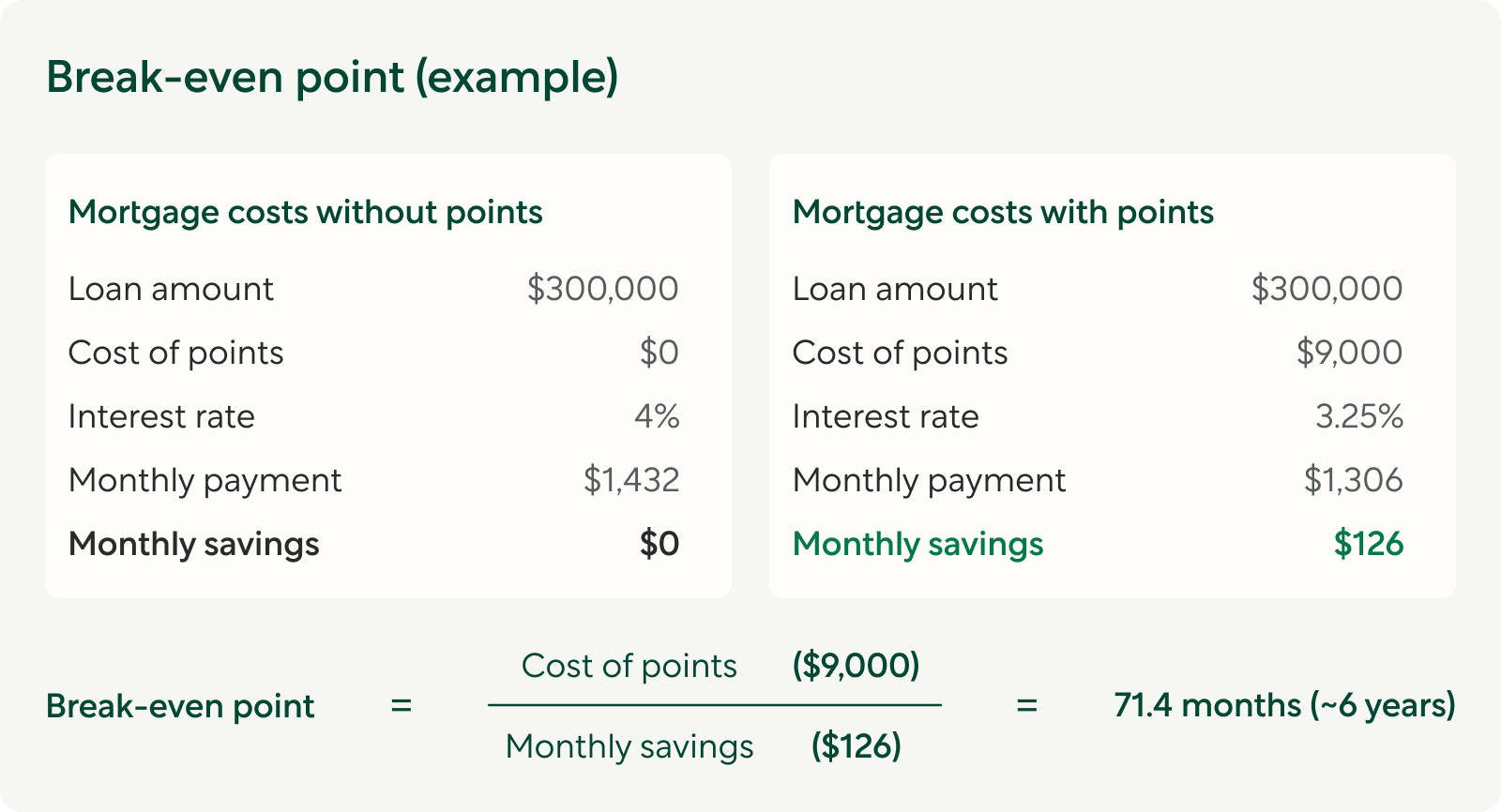

Let’s say you're applying for a $300,000 mortgage at a 4% interest rate, resulting in a monthly payment of $1,432.

If you pay $9,000 for mortgage points, your lender might reduce your interest rate to 3.25%, lowering your monthly payment to $1,306.

That’s a savings of $126 per month.

But how do you know if it’s worth it? You can calculate your break-even point by dividing the cost of the points by your monthly savings. In this case, the break-even point would be:

If you plan on staying in your home for more than six years, paying for the points could be a great deal. If you move or refinance before then, the upfront cost might not be worth it.

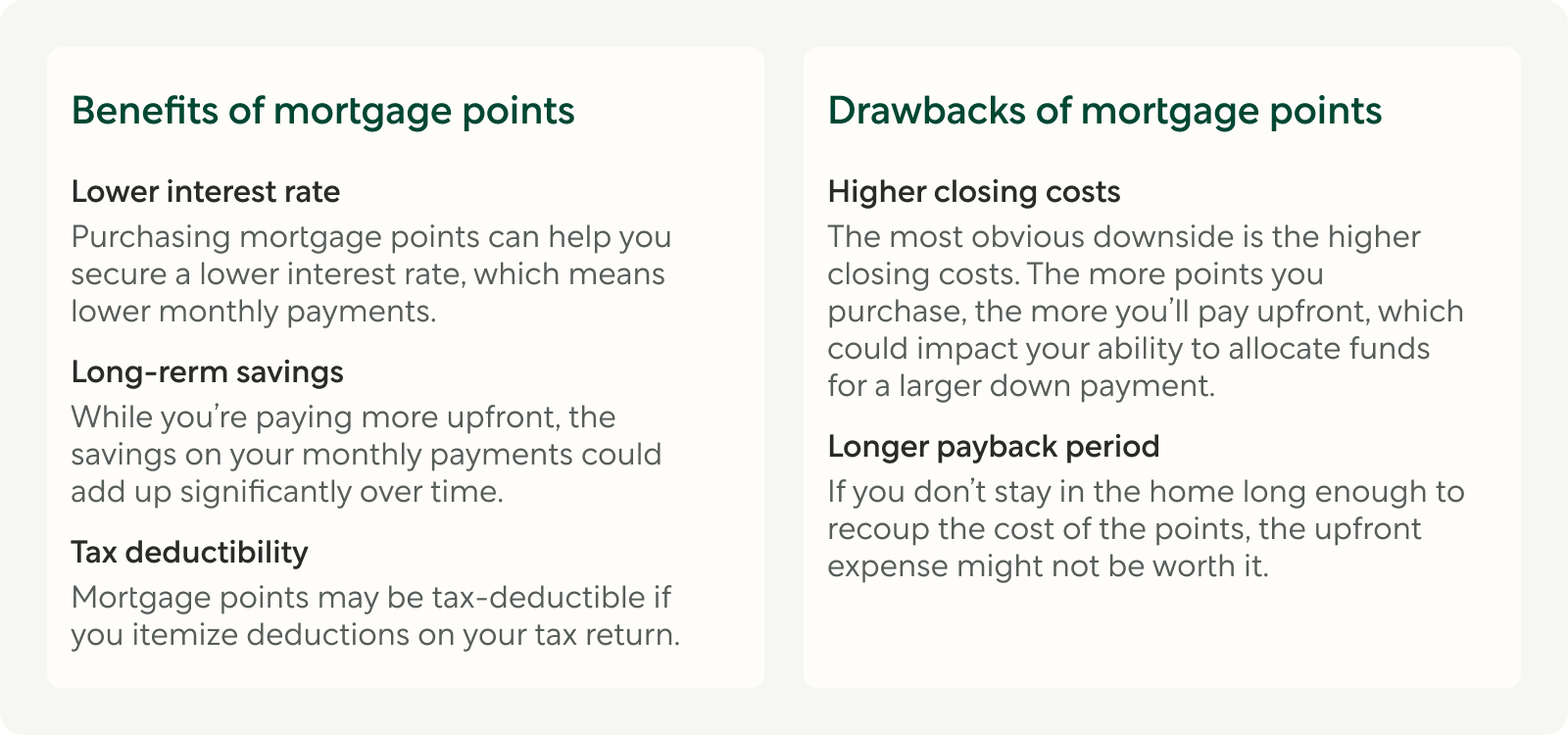

Pros and cons of mortgage points

How to calculate mortgage points?

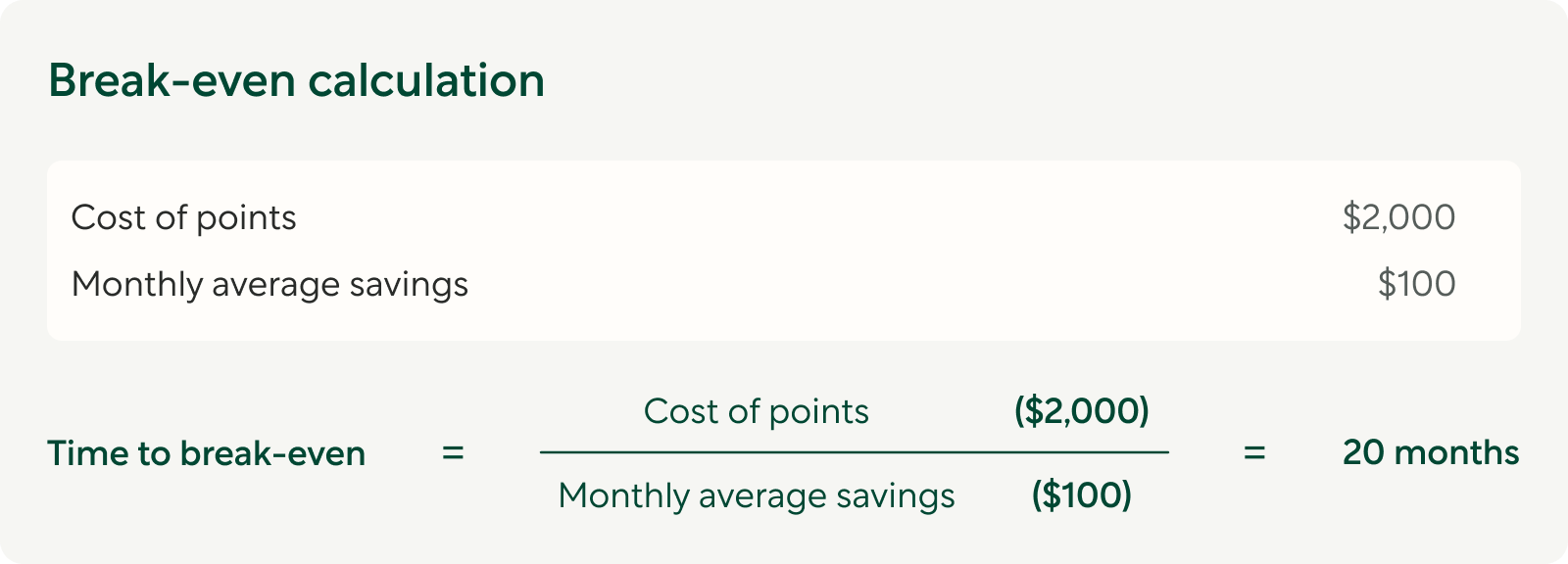

As mentioned, one mortgage point costs 1% of your loan amount. Let’s look at a more specific example: If you're taking out a $200,000 mortgage, one point would cost you $2,000.

To determine whether buying mortgage points is worth it, you’ll need to calculate your break-even period. This is the amount of time it will take for the monthly savings from a lower interest rate to offset the upfront cost of the points.

Breakeven calculation

If you pay $2,000 for points and your monthly savings are $100, it will take you 20 months (or just under two years) to break even:

If you plan to stay in your home for longer than 20 months, buying mortgage points could be a good deal.

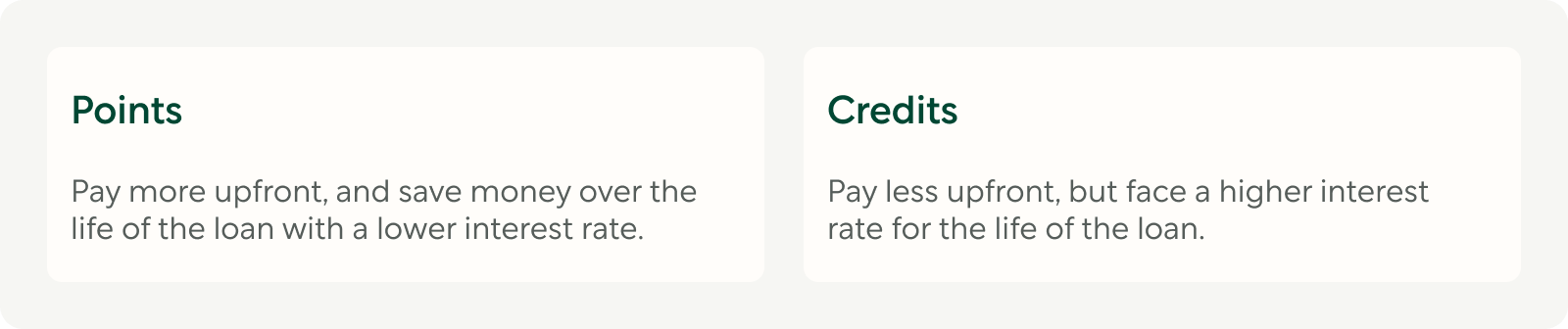

Points vs. credits: what's the difference?

You might also encounter the option of mortgage credits. This is the opposite of purchasing mortgage points. Instead of paying up front for a lower interest rate, you accept a higher interest rate in exchange for the lender covering some of your closing costs.

Choosing between points or credits depends on your financial situation and how long you plan to stay in the home.

Are mortgage points worth it?

Mortgage points might not be ideal for everyone, but they can be a great option in certain scenarios.

When do mortgage points make sense?

At Better Mortgage, we’re here to help you navigate these decisions. We can provide clear answers about mortgage points and help you understand your best options for saving money in the long run.

Ready to get started?

If you're considering buying a home or refinancing your mortgage and want to explore mortgage points, getting pre-approved is the best way to start.

At Better Mortgage, you can get pre-approved in just three minutes—no paperwork or hassle. Reach out today to see how mortgage points can help you save.

Mortgage points FAQs

What are discount points on a mortgage, and how do they work?

Mortgage points are fees that allow you to lower your mortgage interest rate. Typically, one point costs 1% of your loan amount, and each point purchased can reduce your interest rate by about 0.25%. You can purchase more than one point or fractional points.

Which types of loans allow you to purchase mortgage points?

You can purchase mortgage points on most loan types, including conforming loans, Federal Housing Administration (FHA) loans, and jumbo mortgages. However, if you're considering an adjustable-rate mortgage (ARM), points generally apply to the initial fixed-rate period. Be sure to ask your lender how mortgage points will apply in your specific situation.

Can you buy points when refinancing?

Yes, you can buy mortgage points when refinancing. The process is the same as it would be for a home purchase: pay for points upfront to secure a lower interest rate on your new loan.

How many mortgage points can you buy?

There is no standard limit on the number of points you can buy, but each lender sets its maximum. At Better Mortgage, the maximum limit is 2.5 points per loan.