Viral Shah (Better Mortgage’s Head of Capital Markets) explains how an adjustable-rate mortgage works.

Choosing a mortgage type is one of the many decisions a homebuyer needs to make – and it’s a big one. After the 2008 housing crisis, many buyers were wary of adjustable rate mortgages (ARMs). But in instances where you’re planning on selling your home within 10 years, they could be the better option.

Here’s a quick overview of what an adjustable rate mortgage is:

How do ARMs work?

While traditional fixed rate mortgages have the same rate for the entire life of the loan (typically 15, 20, or 30 years), adjustable rate mortgages (ARMs) are a bit different. ARMs have an initial fixed period where you will pay a fixed interest rate, followed by an adjustable period where the interest rate fluctuates. Current conforming ARMs use an index rate called the Secured Overnight Financing Rate (SOFR) to guide these adjustments.

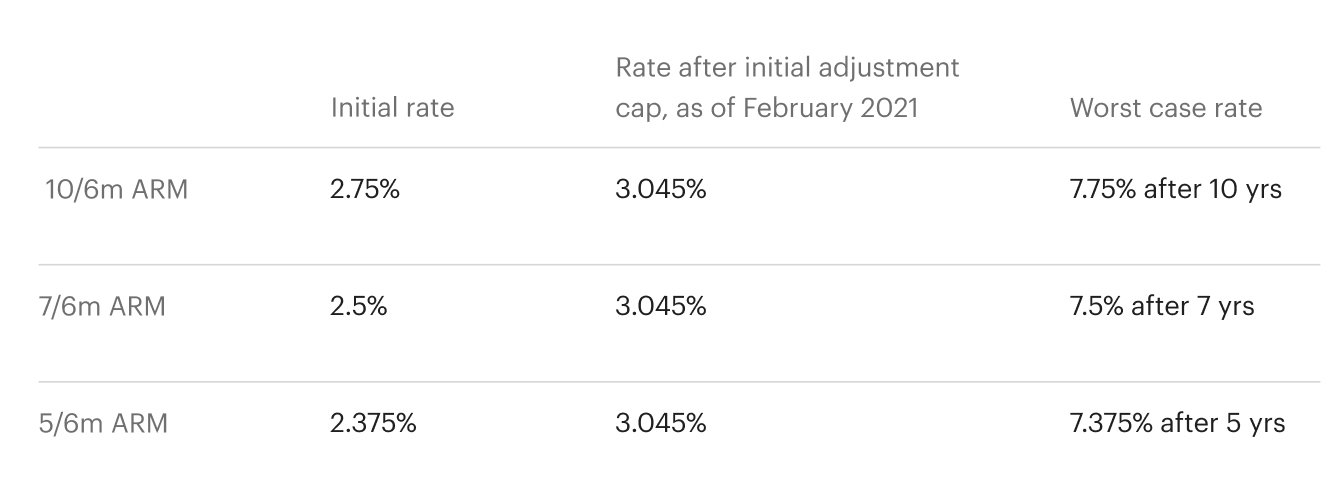

Naming: (Fixed period in years / number of adjustments per year). For example, 10/6m means 10 year fixed with adjustments every 6 months after that.

Fixed period: You’ll choose from a 5-year, 7-year, or 10-year fixed period, typically based on how long you expect to live in the house. After the fixed period, the rate adjusts twice per year (every 6 months).

Adjustable period: After the fixed period is over, the rate will adjust every 6 months based on the following formula: 30 day average of SOFR (Index) + (Margin). Investors set the value of the margin but it is typically between 2.75% and 3%. Regardless of what value is used, the margin always stays the same, but the value of the SOFR index will vary. The SOFR index is maintained by the New York Federal Reserve and can be accessed directly on the NY Fed website or on sites like the Wall Street Journal and its value changes daily. As of 2/22/2021, the 30-day average SOFR was 0.045%, which would mean your ARM loan interest rate could be .045% (Index) + (Margin) or between 2.795% and 3.045%.

How much can the rate move?

ARMs have “caps,” which limit the amount that the rate can increase. This protects you against sharp moves if you move into the adjustable period.

Initial Adjustment Cap: The most the total rate can increase by in the first adjustment period. Typically 2% for 5/6m ARMs and 5% for 7/6m or 10/6m ARMs.

Subsequent Adjustments Cap: The most the total rate can increase by in subsequent adjustments periods. Typically 1%.

Lifetime Adjustment Cap: The most the rate can increase above the initial fixed rate — ever. Typically 5%.

For example: If your initial 5/6m ARM fixed rate was 3%, once the fixed period is over, it can’t increase more than 4% every year, nor can it ever exceed 8% in total.

Example rates based on the current interest rate environment:

This table is for illustrative purposes only.

At Better Mortgage, we recommend considering an ARM only if you’re reasonably certain you’re going to sell your house in 10 years or less: here’s why.

If you’re curious about what ARM rates are like today, take a look at our Rate Quote Tool. We’re here to help you figure out which option is right for you.

This blog is for informational purposes only and should not be used for legal or financial advice.