What You’ll Learn

What title insurance is and why it’s important

Scenarios where title insurance can protect you

The services offered by a title insurance company

Title insurance is a form of insurance that homeowners are required to purchase in nearly all refinance and purchase transactions. Unlike other forms of insurance, title insurance protects borrowers and lenders from issues that occurred in the past rather than issues that may arise in the future.

There are two types of title insurance: a mandatory lender’s policy that covers the lender (e.g., Better Mortgage), and an optional (but highly recommended) owner’s policy that covers the homeowner.

A “title” is a document that states the legal owner of a property. So title insurance protects both mortgage lenders and owners against past defects or problems with the legal ownership of a property. This includes things like forged documents, lien claims on the property, undisclosed easements, ownership claims made by others, and mistakes from the previous title agency.

OK, that’s a lot of obscure terminology, so let’s take a look at a few concrete scenarios. These are some examples of legal headaches that can arise which title insurance can protect you and your lender from:

- You bought your house last year from a seller who inherited the property. However, you find out later that the seller has an undisclosed step-brother who also owns half of the property, according to the will. In this case, title insurance would help you offset the legal costs of challenging his claims to your property.

- You bought a house, but it turns out that the seller had an overdue bill on a previous home addition. Now there’s a mechanic’s lien on the property from several years ago that predates your mortgage. Without title insurance, you’d be held liable as the current homeowner.

- Part of your property turns out to be inaccessible due to a mistake by a past surveyor. Your property records are different than expected and the value of the home is affected as a result. Without title insurance, you wouldn’t be compensated for the financial loss.

Is title insurance required?

There are two types of title insurance policies: a lender’s policy and an owner’s policy. Both types of policies are typically offered as a bundle together.

A lender’s policy is required in every purchase and refinance transaction, and the borrower typically pays for it in a refinance transaction. Should there be a potential title issue, this policy protects only the mortgage lender in the amount of the loan.

On the other hand, an owner’s policy protects the buyer. Although it’s not required by law for borrowers to purchase an owner’s policy, it is highly recommended to make sure that you, as a homeowner, are protected from any potential legal issues that may come up.

How much does title insurance cost?

Before we explain the cost of title insurance, let’s first break down what services title companies offer. Title companies often provide two services during the mortgage process: title insurance and settlement services.

Title insurance is the service that insures the person who is buying or refinancing the house as the rightful owner of the property. This cost is called the “title insurance premium” and is regulated on a state-by-state basis. The premium is a one-time cost paid at closing and can range from 0.50% of the purchase amount to over 1% depending on the state the property is located in. Because it’s a percentage of the purchase amount, your title insurance premium can increase if your loan amount goes up.

Settlement service fees, on the other hand, include the fees that are incurred during closing, such as the cost of escrow and wire fees. This can also include fees for activities involved in underwriting the title insurance policy, such as the title search fee and the cost to resolve issues. Like title premiums, these costs vary by state, but because these fees are charged by the title company itself, these can range from a couple hundred to over $1,000.

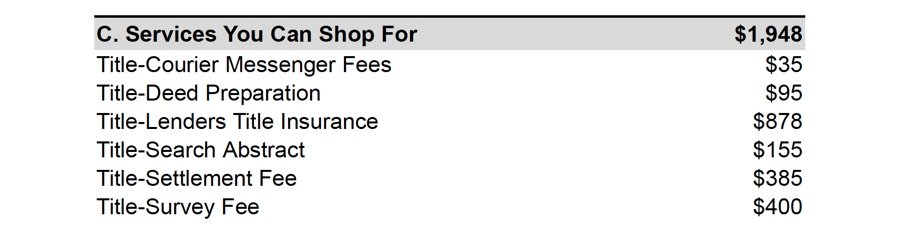

Your expected title and settlement costs can be found in the “Services You Can Shop For” section of your loan estimate. See example below.

“Lender’s title insurance” is the cost of the title insurance premium. All the other costs listed are fees related to settlement.

Note: the example below is for illustration purposes only and is not indicative of the title/settlement costs for your particular scenario.

At Better Mortgage, we have our own affiliated title and settlement services company, Better Settlement Services, whose mission is to provide the best and most seamless service at competitive rates and with transparency.

Still have questions about title insurance? We’re here to walk you through any concerns or answer any questions you might have.