What you’ll learn

How to interpret the numbers attached to a mortgage product

Some of the most important factors to consider when comparing mortgage rates

The importance of transparency when choosing a mortgage lender

As you shop for a mortgage, you’ll notice that most lenders or mortgage rate comparison websites have some version of a rate table on their website. The idea is to provide borrowers with a snapshot of the lender's mortgage products, rates, and estimated monthly payments for a typical home. Rate tables may seem complicated at face value, but they’re one of the best mortgage comparison tools you can use in your search for home financing. Here’s everything you need to know about rate tables, and how to use one to choose the right mortgage for your needs.

How does one lender’s rate table differ from the next?

The first thing to know about rate tables is that no two rate tables are the same. Different lenders offer different loans, terms, and fees—which is why it's crucial to look at multiple rate tables before you make any decisions. What's more, you could review the same rate table over the course of several days and see completely different rates from one day to the next. That’s because interest rates are affected by external factors, such as inflation, economic growth, and the state of the housing market. These variations can be particularly pronounced in times of economic volatility.

Rates also differ between mortgage products. For example, a 30-year fixed-rate mortgage will usually have a higher interest rate than a 15-year fixed-rate mortgage. In this instance, the lender charges a higher interest rate to offset the increased risk of the borrower defaulting during the 30-year loan term. Similarly, a mortgage to refinance a home will almost always have a lower interest rate than a mortgage to purchase a home. That’s because the lender can see that a refinancing borrower has a proven track record of fulfilling their mortgage payments on time.

It’s important to recognize these differences as advertised on rate tables. That way, you can compare lender rates as closely as possible to ensure they’re “apples to apples” and not “apples to oranges” comparisons.

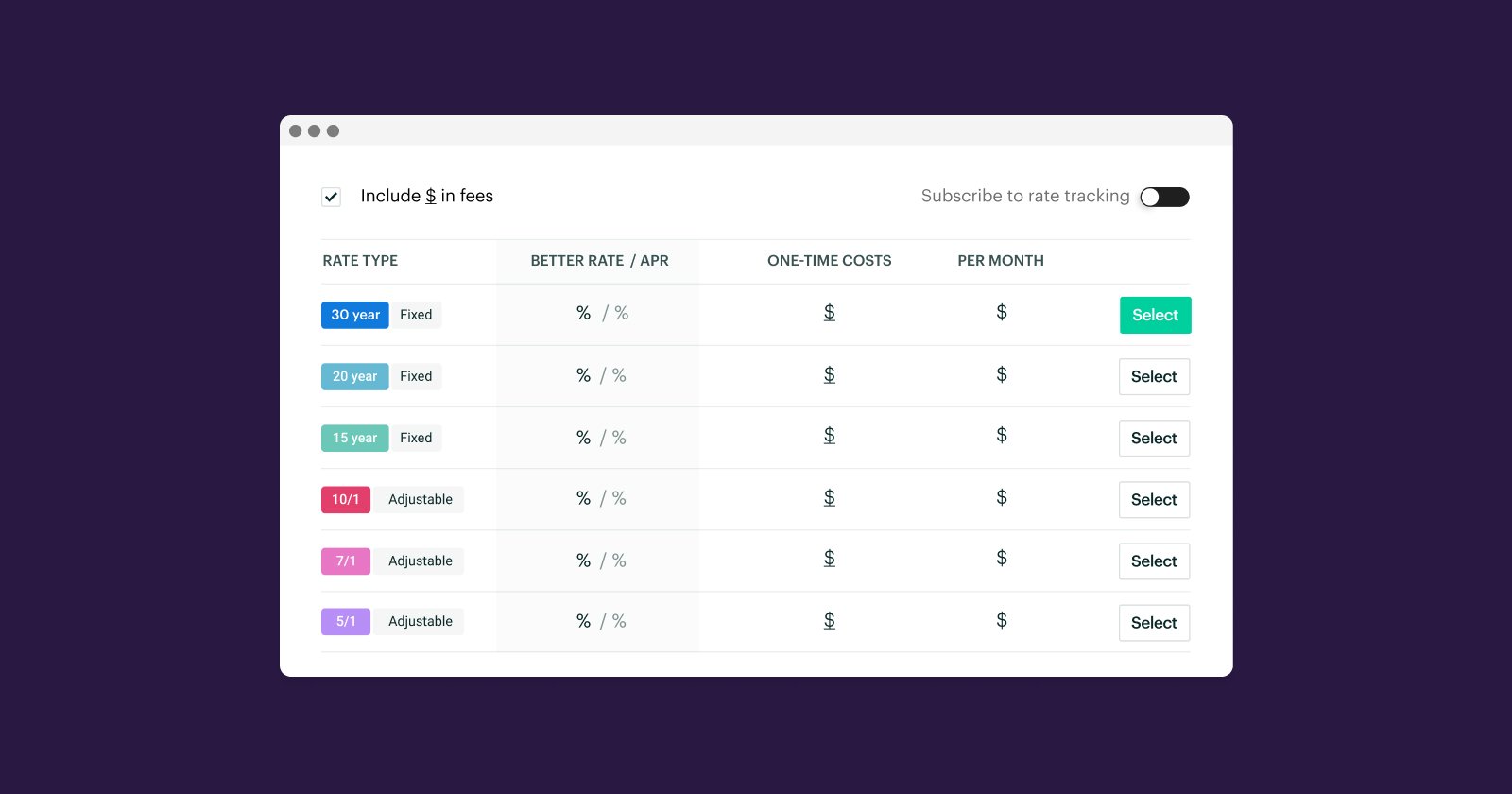

Breaking it down: What do all the numbers mean?

There’s no standard format for how lenders will display rates, but most tend to feature the same kind of information—even if it isn’t laid out exactly the same. When you look at a rate table, here are the important factors to consider.

Disclaimer: For illustrative purposes only

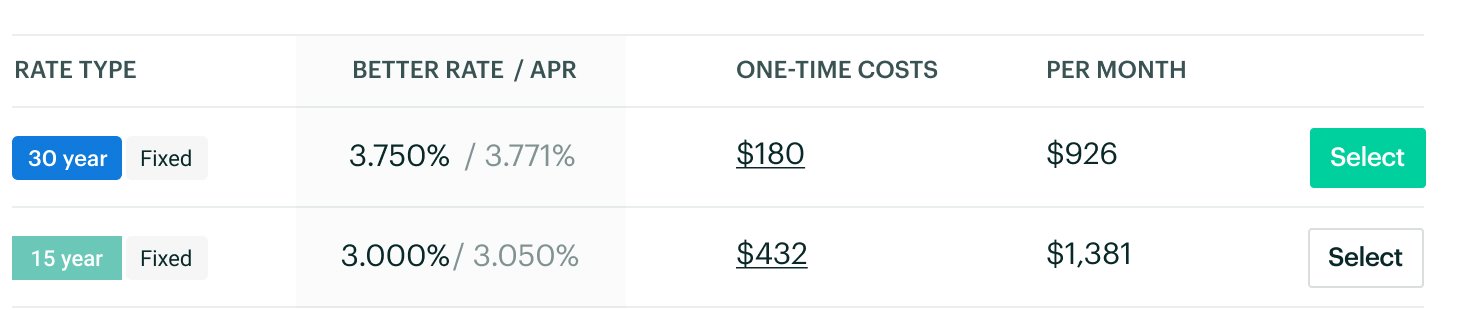

Rate type

The first column of information in a rate table is usually designated to the types of mortgages that the lender is offering, based on the information you provided about your house and financial situation. Here, you can see the loan term (i.e. how long you’ll be making payments before the mortgage is paid in full) and whether the mortgage has a fixed or adjustable interest rate. A fixed-rate mortgage has the same interest rate for the entire life of the loan. An adjustable-rate mortgage (ARM) has a fixed interest rate for an initial period of time, such as the first 5 or 7 years. After that, the interest rate adjusts to reflect market conditions.

Interest rate

Rate tables usually display the best interest rate available for each specified loan. However, the rates you’ll actually qualify for depends on a number of factors—including your credit score, down payment, and the type of property you’re looking to purchase, as well as its location. Check to see if the rate table offers a disclosure section that provides information about the numerical examples and loan scenario used and what’s needed to obtain the displayed rates, or play around with the information and assumptions you input to see how interest rates may change as a result.

Also, keep in mind that the mortgage with the lowest interest rate may have a higher monthly payment. Choosing the right mortgage and interest rate is a holistic decision. You have to figure out if you can afford the monthly payments, if you have the down payment required, if you’ll qualify for the rate—and, more than anything, your personal comfort level.

APR

While many borrowers tend to get caught up on interest rates, it’s the annual percentage rate (APR) that provides the clearest picture of what you’ll actually pay for your mortgage. The APR includes the interest rate plus some closing costs and fees, displayed as a percentage. The inclusion of this information is incredibly helpful because costs and fees can vary substantially between lenders and loan types. For example, two lenders could offer the exact same mortgage product with the exact same interest rate, but the APR on each could be wildly different because one lender charges loan origination fees and the other doesn’t (PS, Better Mortgage doesn’t). Unfortunately, APR is not always displayed on rate tables. If it’s not readily available, make sure to ask your lender for this information before securing your home loan.

Points and credits

Points, also known as discount points, are a one-time fee you can pay to decrease your interest rate. This is what’s known as “buying down” a rate, as you’re literally prepaying interest at closing. In most cases, 1 point costs 1% of the total mortgage amount and discounts 0.25% from the interest rate. Credits are the opposite. In exchange for a higher interest rate, a lender will lower your closing costs—or even pay them completely. Credits can be advantageous for homebuyers on a particularly tight budget or those who are looking to reduce their out of pocket costs at closing.

Whether you take credits or you pay points requires careful consideration. Learn more about how to decide between points and credits with our helpful guide.

Monthly payment

Finally, some lenders will share the estimated monthly payment for each loan. Note that the payment you see often doesn’t include estimates for additional monthly escrow fees, such as homeowners insurance, private mortgage insurance (PMI), and property taxes. These should be factored in separately and can change over time. However, if you have a down payment of 20% or more, you won’t have to pay PMI.

Disclaimer: For illustrative purposes only

Be aware: You may not qualify for an advertised rate

When it comes to mortgage rates, what you see is not always what you get. Being able to obtain a certain interest rate depends on several factors as well as the assumptions used to display the rates advertised. The only guaranteed rate is one that you lock.

Credit score

If your credit score doesn’t meet specific eligibility requirements, you may not qualify for the best advertised rates. For example, a lender may require a minimum credit score of 750 to receive the lowest rate. While some rate tables provide this information in a disclosure section, not all do. In that case, you’ll want to contact that lender directly to learn more.

Down payment

Many rate tables do not display down payment requirements for advertised rates. For example, the lowest interest rates may not be available if you put down less than 20%, even if your credit score is solid.

Other financial considerations

Rate tables won’t account for individual factors such as your debt-to-income ratio, which is another major consideration for mortgage lenders. If you have a bankruptcy or loan in default on your credit score, then you may not qualify for a mortgage at all.

When choosing a lender, look for transparency

Not every mortgage lender provides all the relevant information in a rate table. Some may include the interest rate but not the APR. Others may not disclose the points you have to purchase to receive the interest rate listed.

Lenders may intentionally leave this crucial information out as a bait-and-switch tactic to entice you, even though their mortgage rates may be unattainable for most borrowers—or just incredibly expensive.

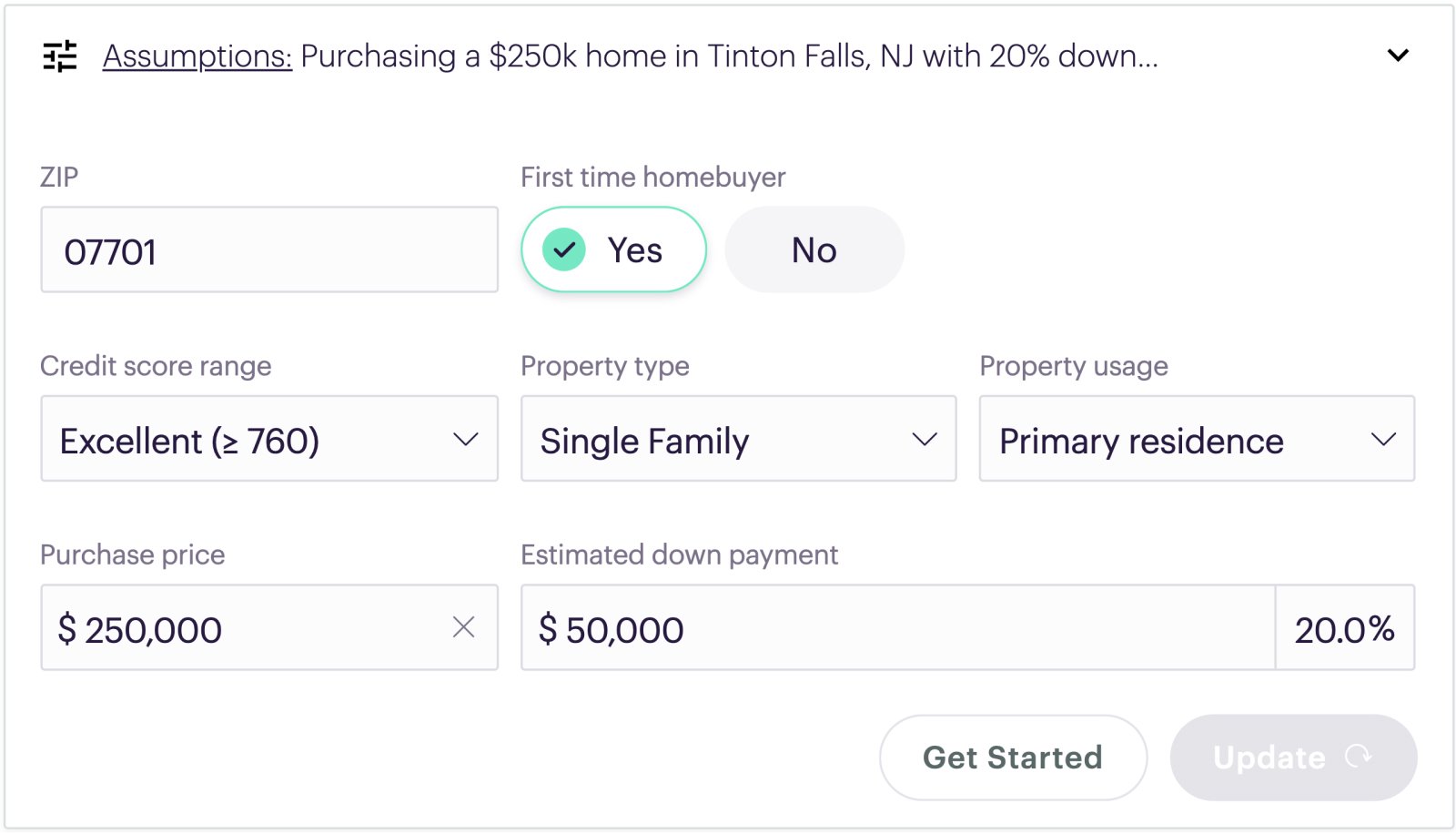

With Better Mortgage, we always disclose APR right in the rate table as well as the assumptions on down payment, credit score, and income that led to the displayed rates.

In fact, you can also customize the rate table to fit your circumstances more accurately by entering your location, home value, down payment, and estimated credit score. In addition, you can input the property type; if the home will be a primary residence, second home, or investment property; and if you’re a first-time homebuyer. These details can make a huge difference in the kind of mortgage offers available to you, and what rates may be available once you qualify.

Disclaimer: For illustrative purposes only

Ready to get started on your mortgage journey? Check out our rates to get a customized estimate based on your unique situation.

Disclaimer: This content is for informational and educational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice.