Paying off student loan debt? You’re not alone — more than 44 million Americans have student loan debt.1 If you’ve made an investment in your education and now want to make an investment in your next home, you might be wondering what your options are. At Better Mortgage, we strive to make homeownership accessible and affordable for all Americans, including those with student debt. As you explore the possibility of homeownership, here are some things to keep in mind.

Student loan. Mortgage. You can have both.

Mortgage lenders don’t look at how much your total student debt is, they look at how much you pay each month towards your loans. To put it into perspective, the average student loan debt in 2020 was $32,731, but as recently as 2019, people were borrowing an average of $37,782 for new cars. For lenders, it’s not about the type of debt you have, they’re more interested in how well you manage your debt.

How will mortgage lenders consider my student debt?

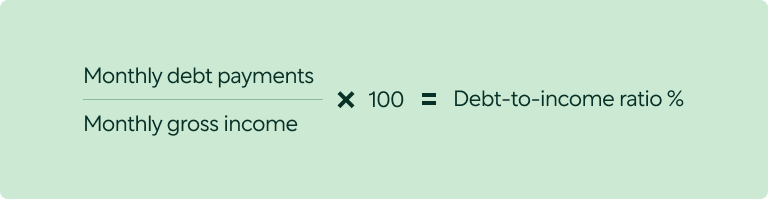

When lenders consider any type of debt, they’ll look at your monthly debt-to-income ratio (DTI). Your debt-to-income ratio is all your monthly debt payments divided by your gross monthly income. In other words, we add up payments for things like credit card debt, an auto loan payment, and your monthly student loan payment and combine that with your future mortgage payment. Then we divide that number by your gross monthly income, which is how much money you earn before taxes. (Keep in mind that if you’ve deferred your student loan payments, we’ll still have to count your future monthly student loan payments towards your DTI.)

The DTI equation

Obtaining a mortgage with student loan debt

Understanding your DTI can help you identify ways to make yourself a more attractive borrower to a lender. At Better Mortgage, we accept DTI up to 50% for creditworthy borrowers, but the lower your DTI, the more home financing options will be available to you. If you can reduce the monthly amount you have to pay to cover your debt commitments by refinancing your student loans or paying off a credit card or two, this can help lower your DTI and increase your financing options. Additionally, if someone else is helping you with your student loan payments, say your parents or a fairy godmother has stepped in to make the payments for you, we may be able to qualify you for a mortgage without even counting your student debt payment in your DTI. Here are more tips on how to improve your DTI.

How much savings do I need to buy a home?

Odds are, your student loan payments have also impacted your ability to save, making it hard to imagine having the money for a down payment or to cover closing costs. While you might have heard that you need to put 20% down to buy a home, that’s just a myth. Better Mortgage offers low down payment options starting with as little as 3% down. In fact, 72% of our buyers put less than 20% down on their homes.

There can also be upfront costs to buying a home beyond the down payment. If you don’t have enough cash to bring to closing, you may be able to roll the closing costs into your loan for a “no cost” mortgage, in exchange for a higher interest rate. At Better Mortgage, we don’t charge any lender or commission fees, so you won’t have to worry about paying for those additional costs if you work with us.

What mortgage loan option is right for me?

Ultimately, if you’re shopping for a home and have student loan debt, it's always a good idea to talk to a lender. According to a 2015 study by Zillow, the relationship between student loans and homeownership is seemingly nonexistent. So student loans should be nothing to stop you. No matter how close you are to buying a home, at Better Mortgage our non-commissioned loan experts can help shine a light on your best path to homeownership. In as little as 3 minutes, Better Mortgage will show you how much you’re likely to be approved for and match you with a loan consultant to talk through your options.